If you own rental property, the “Great Reset” is likely on your mind. Many investors who locked in historic lows a few years ago are now staring down a renewal notice with rates that look significantly different.

When your mortgage payment climbs but your rental income stays steady, that once-comfortable cash flow can turn thin—or even negative—overnight. But before you consider offloading a long-term asset, there are several strategic ways to bridge the gap.

The Reality of Today’s Market

The shift from 2-3% rates to current market levels is a significant hurdle. For a typical investment property, this can mean a monthly payment increase of hundreds, if not thousands, of dollars.

The goal right now isn’t necessarily to find the “lowest rate” in history, but to optimize your debt structure to protect your monthly liquidity.

Three Ways to Improve Your Cash Flow

If your renewal is approaching in the next 6–12 months, consider these maneuvers:

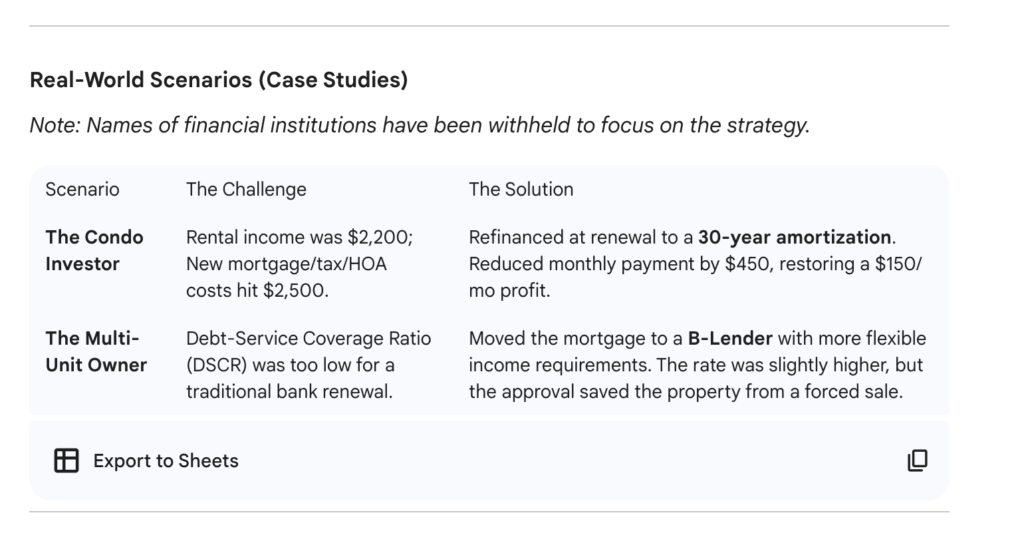

• Re-Amortization: If you have built up equity, we can look at “stretching” your remaining balance back out to a 30-year amortization even 40 years. While this increases the total interest paid over the life of the loan, it significantly lowers your immediate monthly obligation, keeping your business cash-flow positive.

• Rental Offset Optimization: Not all lenders treat rental income the same way. Some use a “Rental Worksheet” that only credits 50% of your rent, while others use a “Net Rental Offset” which is much more generous. Switching to a lender with a more favorable offset can help you qualify for better terms or additional financing.

• The “Hybrid” Approach: Some investors are choosing shorter terms (1–2 years) or even adjustable rates. The bet here is that if rates soften in the near future, you aren’t locked into a high 5-year fixed rate, allowing you to pivot sooner.

Real-World Scenarios (Case Studies)

Note: Names of financial institutions have been withheld to focus on the strategy

Why Proactive Planning Matters

Waiting for your bank’s renewal letter 30 days before the deadline is a recipe for stress. Most lenders will simply offer you their “posted” rate, which is rarely the most competitive option for an investor.

By looking at your portfolio now, we can run the numbers on multiple lenders to see who offers the best rental income treatment and flexibility.

Pro Tip: Your mortgage is a tool, not just a debt. In a high-rate environment, the “best” mortgage is the one that keeps your portfolio sustainable until the market cycles again.

Let’s Run Your Numbers

Don’t let a renewal notice dictate your investment strategy. Whether you want to explore re-amortization or see which lenders are currently “investor-friendly,” I’m here to help.

Leave a Reply