Commercial Mortgage Broker Vancouver | Expert Financing for Warehouses, Offices, Retail, Hotel & Multi-Family | Morning Lee

Leading commercial mortgage broker securing loans for warehouses, offices, retail, plaza, stripe mall, hotels & multi-family properties. Get tailored financing solutions with competitive rates.

Vancouver’s Premier Commercial Mortgage Broker

*Funded for Industrial, Retail & Hospitality Properties*

Why 87% of Vancouver Investors Choose a Specialized Commercial Mortgage Broker

Navigating commercial financing requires expertise in:

- Asset-Specific Underwriting: Warehouse clearance heights vs hotel occupancy metrics

- Market Cycle Timing: Capitalizing on cap rate fluctuations

- Complex Deal Structuring: CMHC-insured multi-family vs conventional industrial loans

- Zoning-Driven Valuations: Industrial vs mixed-use premiums

Commercial Property Financing Solutions

Tailored Mortgage Structuring by Asset Class

Warehouses & Industrial Facilities

Financing for last-mile logistics, manufacturing & distribution

- Clearance height premium financing

- Power supply infrastructure loans

- Cross-dock facility specialized programs

Office Buildings

Downtown core towers to suburban flex spaces

- Tenant improvement allowance financing

- Green building certification incentives

- Vacancy rate bridge solutions

Retail Stores & Shopping Centers

Anchor tenant-dependent financing strategies

- Pad site construction loans

- Renovation financing during tenant turnover

- Sales volume-based underwriting

Multi-Family Buildings

*5+ unit apartment building expertise*

- CMHC-insured refinancing

- Value-add repositioning loans

- Rent roll analysis optimization

Hotels & Hospitality

Occupancy-driven financing solutions

- RevPAR-based underwriting

- Renovation PIP financing

- Seasonal cash flow accommodations

Plaza and Strip Malls

Financing anchored retail centers and neighborhood plazas

- Anchor tenant credit analysis (national vs local)

- Pad site acquisition and development loans

- Renovation financing for tenant retention

- Vacancy rate bridge solutions during repositioning

- Sales volume-based loan covenants

- Outparcel financing opportunities

- CAM cost recovery underwriting

Special Purpose Properties

Unique asset financing

- Automotive service centers

- Self-storage facilities

- Gas stations/C-stores

The Commercial Mortgage Broker Advantage

Why Developers & Investors Partner With Us

Access to 1100+ products / Lender Channels

- Big 6 Banks

- Credit Unions

- Private Funds

- CMHC Providers

Deal Engineering Expertise

Rate Negotiation Mastery

- Average 0.92% lower rates than direct bank offers

- 30-120 day rate hold guarantees

- Pre-approval leverage for off-market acquisitions

Our Commercial Mortgage Process

Four-Phase Approval Framework

- Asset Strategy Session

- Property type-specific underwriting assessment

- Cash flow optimization analysis

- Lender Matchmaking

- institution pre-screening

- Loan scenario modeling (term, amortization, covenants)

- Submission Crafting

- Bank-grade proposal packaging

- NOI enhancement documentation

- Closing Coordination

- Legal/tax specialist integration

- Draw administration for construction loans

Why Vancouver’s Top Developers Trust Our Commercial Mortgage Broker Team

Quantifiable Expertise

- 30+ years team financing Vancouver commercial real estate

- High approval rate on complex deals

- Portfolio financing for many business owners and investors

Client Protection Framework

- No upfront broker fees

- Full lender fee transparency

- Ongoing rate monitoring

- Refinancing advantage alerts

Start Your Commercial Financing Journey

Step 1: Property Assessment

Step 2: Lender Matching

Book Asset Strategy Call

Step 3: Loan Structuring

“While banks see property types, we see potential. Let us unlock your asset’s financing power.”

— Commercial Mortgage Broker Morning Lee

Resources:

-

Helping Family Members Buy Homes: A Living Inheritance Through Reverse Mortgage

For many families, supporting the next generation in buying real estate has become both a dream and a challenge. Housing prices keep climbing, down payments feel heavier than ever, and traditional financing doesn’t always offer the flexibility people need. This is where a little-known tool can make a big difference: using a reverse mortgage as a form of living inheritance.

A living inheritance simply means parents or grandparents provide financial support while they are still alive, instead of waiting until an estate is transferred. For families, this approach can be life-changing. Imagine helping your child secure the down payment for a first home, or giving them the freedom to invest in a property they couldn’t otherwise reach—without needing to sell your own investments or create an unexpected tax bill.

Here’s how it works. Many homeowners are asset-rich but cash-poor. They may not have liquid assets, or may not qualify for a traditional mortgage or a home equity line of credit (HELOC). A reverse mortgage opens another door: it allows homeowners to release equity directly from their primary residence. The funds are tax-free and, most importantly, payment-optional. That means no mandatory monthly principal and interest obligations, keeping financial stress low.

Why does this matter? Because gifting from taxable investments often triggers capital gains tax and reduces long-term savings. By borrowing against the home, families can often lower their overall cost while still passing on meaningful support. It’s not about spending the house; it’s about using existing equity as a financial tool, so parents can help their children today while still enjoying the home they love.

This strategy is increasingly seen as a way to balance personal retirement needs with the desire to give. Instead of selling off investments or downsizing too soon, a reverse mortgage can act as a flexible, cost-efficient cushion that aligns family goals with financial reality.

For those curious about practical examples, the concept is explored further in Reverse mortgages: 55+? A cushion against the rising cost of living,

When it comes to real estate decisions—whether buying, selling, or planning financing options—it helps to know all the tools available. MorningLee.ca is where knowledge and opportunity meet.

-

Turning Home Equity Into Opportunity: Why More Canadians Are Exploring Reverse Mortgages

For many homeowners, the family house is more than just a roof overhead—it is often their largest single asset. Over time, as mortgages are paid down and property values rise, the equity in a home can quietly grow into a powerful financial tool. Increasingly, Canadians are discovering ways to unlock that equity to achieve goals that once seemed out of reach: buying a vacation property, helping adult children enter the market, or strengthening retirement income.

Reverse Mortgage Basics

A reverse mortgage is designed specifically for homeowners aged 55 and older. Unlike a traditional mortgage, it does not require mandatory monthly principal or interest payments. Instead, repayment is deferred until the borrower sells the home, moves, or passes away. The loan amount is determined by several factors including the homeowner’s age, property value, and location. Because there are no mandatory payments, borrowers often see their Total Debt Service ratio (TDS) reduced—an important factor when lenders evaluate overall borrowing capacity.

For those who want to dig deeper into how reverse mortgages can cushion against rising living costs, a detailed overview is available here: Reverse mortgages: 55+? A cushion against the rising cost of living.

Applications Beyond Retirement

Traditionally, reverse mortgages have been seen mainly as a retirement planning tool. But in today’s real estate market, some homeowners are leveraging them for broader purposes. For example, funds released from a principal residence can be used to:

- Purchase a second home or vacation property, either outright or in combination with a traditional mortgage.

- Invest in a rental property to generate supplemental income.

- Support lifestyle choices such as downsizing at the right time without rushing to sell in a slower market.

Because reverse mortgages do not impose the same monthly repayment obligations, homeowners may find themselves eligible for additional borrowing opportunities that would otherwise be out of reach.

Balancing Investment and Risk

Using home equity as leverage can open doors, but it comes with important considerations. Tax implications—such as capital gains on second properties or reporting rental income—need careful planning. Market risks, including price fluctuations and potential vacancies, also play a role. On the other hand, for those with a long-term horizon, real estate remains a tangible asset that can diversify overall retirement strategy.

A Smarter Approach to Real Estate Planning

What makes these strategies appealing is flexibility. Some homeowners choose to hold onto their existing property while purchasing a new one, postponing the sale until market conditions align with their goals. Others appreciate the low prepayment penalties available in certain reverse mortgage products, giving them freedom to adjust plans as life changes.

Real estate decisions—whether buying, selling, or financing—are rarely one-size-fits-all. They require careful evaluation of financial position, lifestyle goals, and long-term outlook. For many Canadians, reverse mortgages have quietly become a tool worth considering in that equation.

To explore more insights and options tailored to your situation, visit MorningLee.ca.

-

Tariff Turmoil Takes Its Toll

Statistics Canada released Q2 GDP data, showing a weaker-than-expected -1.6% seasonally adjusted annual rate, in line with the Bank of Canada’s forecast, but a larger dip than the consensus forecast. The contraction primarily reflected a sharp decline in exports, down 26.8%, which reduced headline GDP growth by 8.1 percentage points. Business fixed investment was also weak, contracting 10.1%, mainly due to a 32.6% decline in business equipment spending.

Exports declined 7.5% in the second quarter after increasing 1.4% in the first quarter. As a consequence of United States-imposed tariffs, international exports of passenger cars and light trucks plummeted 24.7% in the second quarter. Exports of industrial machinery, equipment and parts (-18.5%) and travel services (-11.1%) also declined.

Amid the counter-tariff response by the Canadian government to imports from the United States (which has now been rescinded), international imports declined 1.3% in the second quarter, following a 0.9% increase in the previous quarter. Lower imports of passenger vehicles (-9.2%) and travel services (-8.5%; primarily Canadians travelling abroad) were offset by higher imports of intermediate metal products (+35.8%), particularly unwrought gold, silver, and platinum group metals.

Export (-3.3%) and import (-2.3%) prices fell in the second quarter, as businesses likely absorbed some of the additional costs of tariffs by lowering prices. Given the larger decline in export prices, the terms of trade—the ratio of the price of exports to the price of imports—fell 1.1%.

But the report was not all bad news. Consumer resilience was also evident. Household consumption spending accelerated in Q2. Personal spending rose 4.5% compared to 0.5% in Q1. Government spending also notably contributed to growth.

An improvement in housing activity also added to economic activity. Residential investment grew at a firm rate of 6.3%, compared to a decline of 12.2% in the first quarter of the year.

Final domestic demand rose 3.5% annualized, reflecting resilience and perhaps Canadians’ boycott of US travel or US products. However, income growth was up just 0.7% year-over-year (at an annual rate), which pulled the savings rate down one percentage point to 5.0%, potentially hampering consumers’ ability to continue their spending.

Inventories of finished goods and inputs to the production process increased by 26.9%, reflecting the Q1 stockpiling of goods that would be subject to future tariffs.

While Q2 was soft, June GDP was arguably more disappointing at -0.1% m/m, two ticks below consensus. Manufacturing was the surprise, falling 1.5%. Services were mixed, with gains in wholesale and retail offsetting some broader weakness. The July flash estimate was +0.1% (on the firmer side, given some of the soft data thus far), but the June figure makes it clear that the final print can be quite different.

The Bank had Q2 GDP at -1.5% in their July Monetary Policy Report, so the miss was minor. And, the strength in domestic demand highlights the economy’s resilience. One negative is that Q3 is tracking softer than their +1% estimate (closer to +0.5%), but it’s still very early, and things can change materially.

Bottom Line

The odds are no better than even for the Bank of Canada to cut rates when they meet again on September 17. There are two key data releases before then — the August Labour Force Survey, released August 5, a week from today, and the August CPI release on September 16. We would have to see considerable weakness in both reports to trigger a Canadian rate cut next month.

A Fed rate cut is far more likely, as telegraphed by Chair Jay Powell at the annual Jackson Hole confab. The battle between the White House and the Fed has intensified with President Trump’s firing of Governor Lisa Cook, the first Black woman on the Board and a Biden appointee. If Trump were to succeed, it would enable him to appoint a majority of the Federal Reserve Board, potentially allowing him to dictate monetary policy.

Trump wants significantly lower interest rates in the US, but even if he succeeds, only shorter-term rates would decline. The loss of Fed independence could lead to higher, longer-term interest rates, which could likely result in higher fixed mortgage rates in Canada. Moreover, inflation pressures could intensify, leading to continued upward pressure on bond yields and diminishing the potential appeal of floating-rate mortgage loans.

Dr. Sherry Cooper

-

Reverse mortgages: 55+? A cushion against the rising cost of living

Did you know?

A reverse mortgage can be a flexible tool for a senior to offset the rising cost of living, to borrow more than a bank may be willing to lend for a traditional mortgage, and to provide emergency funds for long-term care.

Scenario

Judith is a 75-year-old and living on Steeles Avenue in North York, Toronto. She’s lived in her home for over 40 years, and she and her late husband raised their family there. Given the location, she figures her older home is worth about $2 million. There’s also been speculation that there may someday be approval for condo development, which could cause the land value to skyrocket.

Judith receives the maximum CPP pension of about $1,300 per month (a combination of her own retirement pension and a survivor pension for her late husband) and gets nearly the maximum OAS pension—another $700 or so each month. That equates to about $2,000 of monthly pension income from the federal government. She also has a small defined benefit pension from the UK government that fluctuates year to year based on the exchange rate.Beyond that, she’s been drawing down a savings account from a modest inheritance from her parents and a small life insurance policy paid out when her husband passed away a few years ago.

Judith’s financial options to help cushion the impact of inflation:

- Credit card

- HELOC

- Sell her home and move into an apartment or retirement home, and invest into GICs to cover her monthly costs.

Solution

Judith decides a reverse mortgage might be a good fit for her—but not yet. She can use the $100,000 secured line of credit from the bank for now, but if she wants to stay in her home, eventually a reverse mortgage might be the best borrowing option. She’s willing to pay interest, and besides, she’s hopeful her home value will rise, tax-free, despite the interest she may pay.

More importantly, depleting the value of her estate seems unfounded. If she sells her home and rents, she’ll be spending a portion of her children’s inheritance either way. Her kids are supportive of her doing what she wants, which is to maintain the status quo.

Judith thinks a lot about what she would want to happen if her health deteriorated. She’d rather not count on help from her kids, preferring to pay for her costs herself.

A reverse mortgage could provide her with roughly $900,000 that could be accessed all at once, advanced as scheduled monthly payments like a pension, or borrowed on an as-needed basis. She may not need to borrow much to supplement her spending in her 80s, but having access to a large part of her home equity appeals to her.

Plus, if a developer does buy along her street to make way for condos, her home value may appreciate significantly.

Ready to Get Started?

If you’d like to learn more about how a reverse mortgage may similarly suit your needs, I’d be happy to help answer any quesitons you may have – with no obligations. Contact Us now.

-

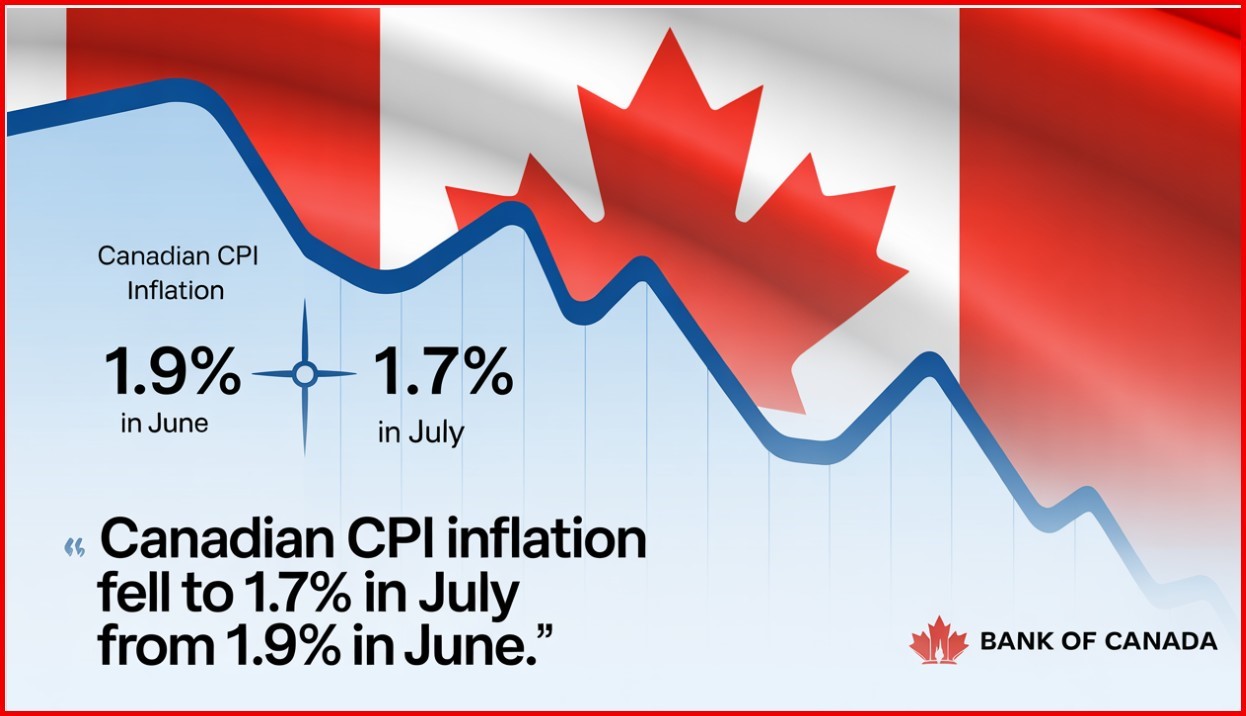

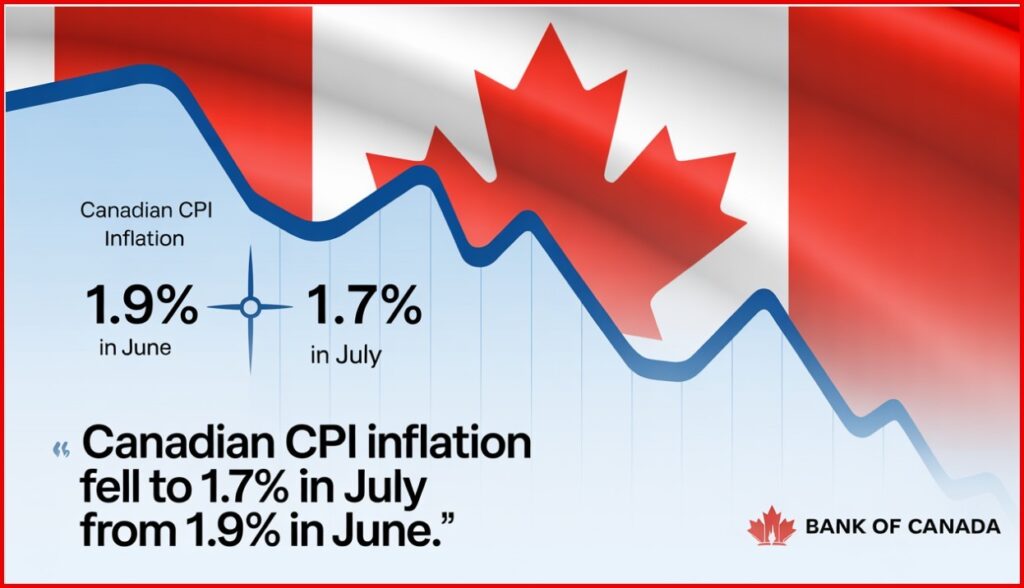

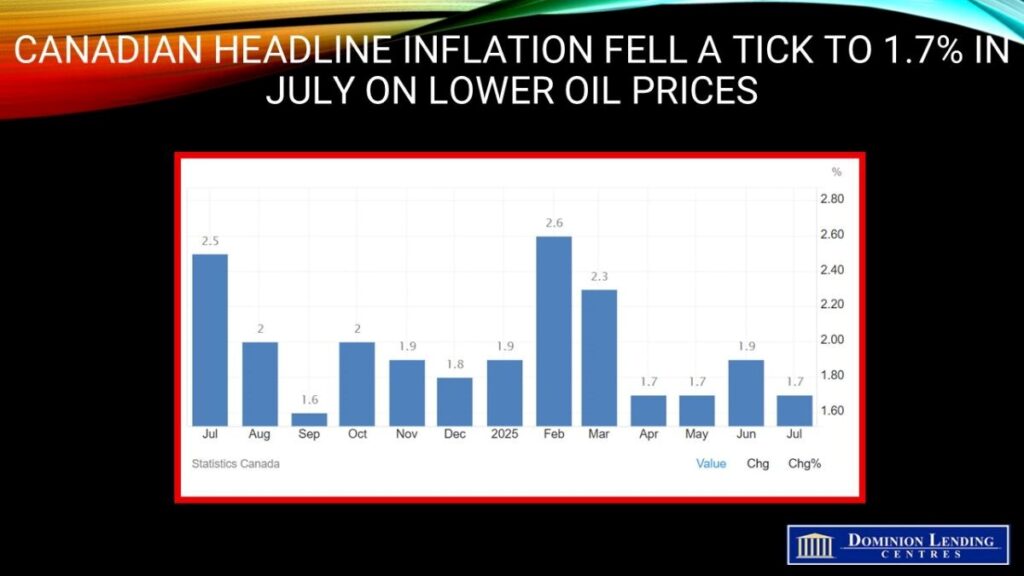

CPI Report Shows Headline Inflation Cooling, But Core Inflation Remains Troubling

Canadian consumer prices decelerated to 1.7% y/y in July, a bit better than expected and down two ticks from June’s reading.

Gasoline prices led the slowdown in the all-items CPI, falling 16.1% year over year in July, following a 13.4% decline in June. Excluding gasoline, the CPI rose 2.5% in July, matching the increases in May and June.Gasoline prices fell 0.7% m/m in July. Lower crude oil prices, following the ceasefire between Iran and Israel, contributed to the decline. In addition, increased supply from the Organization of the Petroleum Exporting Countries and its partners (OPEC+) put downward pressure on the index.

Moderating the deceleration in July were higher prices for groceries and a smaller year-over-year decline in natural gas prices compared with June.

The CPI rose 0.3% month over month in July. On a seasonally adjusted monthly basis, the CPI was up 0.1%.

In July, prices for shelter rose 3.0% year over year, following a 2.9% increase in June, with upward pressure mostly coming from the natural gas and rent indexes. This was the first acceleration in shelter prices since February 2024.

Prices for natural gas fell to a lesser extent in July (-7.3%) compared with June (-14.1%). The smaller decline was mainly due to higher prices in Ontario, which increased 1.8% in July after a 14.0% decline in June.

Rent prices rose at a faster pace year over year, up 5.1% in July following a 4.7% increase in June. Rent price growth accelerated the most in Prince Edward Island (+5.6%), Newfoundland and Labrador (+7.8%) and British Columbia (+4.8%).

Moderating the acceleration in shelter was continued slower price growth in mortgage interest cost, which rose 4.8% year over year in July, after a 5.6% gain in June. The mortgage interest cost index has decelerated on a year-over-year basis since September 2023.

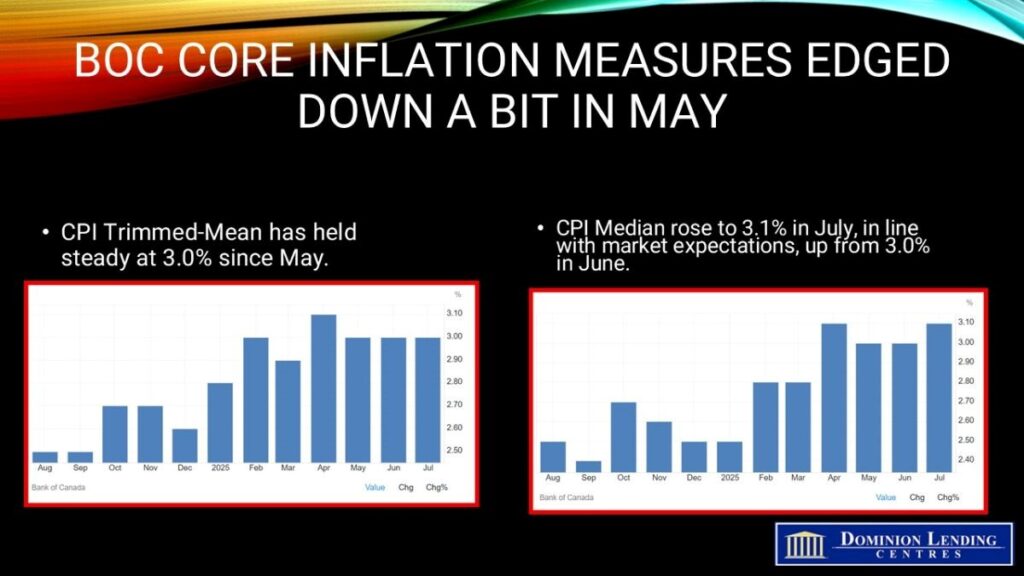

The Bank of Canada’s two preferred core inflation measures accelerated slightly, averaging 3.05%, up from 3% in May, and above economists’ median projection. Traders see the continued strength in core inflation as indicative of relatively robust household spending.

There’s also another critical sign of firmer price pressures: The share of components in the consumer price index basket that are rising by 3% or more — another key metric the central bank’s policymakers are watching closely — expanded to 40%, from 39.1% in June.

CPI excluding taxes eased to 2.3%, while CPI excluding shelter slowed to 1.2%. CPI excluding food and energy dropped to 2.5%, and CPI excluding eight volatile components and indirect taxes fell to 2.6%.

The breadth of inflation is also rising. The share of components with the consumer price index basket that are increasing 3% and higher — another key metric that the bank’s policymakers are following closely — fell to 37.3%, from 39.1% in June.

Bottom Line

With today’s CPI painting a mixed picture, the following inflation report becomes more critical for the Governing Council. The August CPI will be released the day before the September 17 meeting of the central bank. There is also another employment report released on September 5.

Traders see roughly 84% odds of a Federal Reserve rate cut when they meet again on Sept 17–the same day as Canada. Currently, the odds of a rate cut by the BoC stand at 34%. Unless the August inflation report shows an improvement in core inflation, the Bank will remain on the sidelines.

Dr. Sherry Cooper