Refinancing Experts | Residential & Commercial Mortgage Solutions | Morning Lee

Expert refinancing solutions for homeowners and businesses. Lower rates, access equity, and consolidate debt. Get personalized refinancing strategies today.

Unlock Your Property’s Financial Potential Through Strategic Refinancing

What Is Refinancing?

Refinancing replaces your existing mortgage with a new loan, typically to:

- Secure lower interest rates

- Access home/property equity

- Consolidate high-interest debt

- Change loan terms (amortization period)

- Switch from variable to fixed rates (or vice versa)

Real Example: Commercial landlord accessed $1.2M equity to acquire adjacent property through refinancing

Why Consider Refinancing?

Residential Benefits

- Rate Reduction: Save 0.5-2.5% on current market rates

- Debt Consolidation: Combine credit cards/loans into lower-interest mortgage

- Renovation Funding: Access up to 80% of current home equity

- Mortgage Optimization: Adjust amortization for cash flow needs

Commercial Advantages

- Portfolio Restructuring: Consolidate multiple properties into single loan

- Value-Add Capital: Fund renovations to increase NOI

- Cash Flow Relief: Extend amortization periods

- Bridge Financing: Secure funds for new acquisitions

Our Process

*4-Step Framework for Optimal Results*

- Equity & Savings Analysis

- Current valuation assessment

- Break penalty calculation

- Rate comparison across lenders

- Solution Architecture

- Debt consolidation planning

- Cash-out refinancing structuring

- Term optimization strategy

- Lender Negotiation

- Rate discount securing

- Fee waivers (appraisal, legal)

- Covenant flexibility

- Seamless Transition

- Legal coordination

- Payout management

- Post-refinance rate monitoring

Why Choose Morning Lee for Refinancing?

Rate Reduction Mastery

Equity Access Expertise

- Residential: Up to 100% loan-to-value

- Commercial: Up to 100% LTV loan to value

- Portfolio: Cross-collateralization strategies

Break Cost Mitigation

- High success rate in penalty negotiation/reduction

- Blended rate solutions

- Portability strategies

Specialized Solutions

- Commercial:

- NOI improvement refinancing

- Zoning change value capture

- Anchor tenant lease leveraging

- Residential:

- Credit repair refinancing

- Rental property cash flow optimization

- Construction draw management

When Refinancing Makes Strategic Sense

| Scenario | Residential Solution | Commercial Solution |

|---|---|---|

| Rates Drop 0.75%+ | Rate term reduction | Interest cost arbitrage |

| Property Value Rises | Equity access for renovations | Portfolio expansion capital |

| Credit Score Improves | Prime rate qualification | Covenant requirement reduction |

| Business Needs Change | N/A | Equipment financing roll-in |

Start Your Equity Taking Out Journey

Step 1: Savings Assessment

Calculate Your Refinancing Savings

Step 2: Strategy Session

Book 15-min Refinancing Audit

Step 3: Application Process

*”We’ve optimized many people through strategic refinancing – let our expertise unlock your property’s financial potential.”*

— Mortgage Expert – Morning Lee

-

Bank of Canada Lowers Policy Rate to 2.5%

Today, the Bank of Canada lowered the overnight policy rate by 25 bps to 2.5% as was widely expected. Following yesterday’s better-than-expected inflation report, the Bank believes that underlying inflation was 2.5% year-over-year.

Through the recent period of tariff turmoil, the Governing Council has closely monitored the risks and uncertainties facing the Canadian economy. Three developments triggered the Bank’s rate cut. Canada’s labour market softened further. Upward pressure on underlying inflation has diminished, and there is less upside to risk to future inflation with the removal of most retaliatory tariffs by Canada.

Considerable uncertainty remains. However, with a weaker economy and less upside risk to inflation, the Governing Council deemed that a reduction in the policy rate was appropriate to better balance the risks going forward.

“The Bank will continue to assess the risks, look over a shorter horizon than usual, and be ready to respond to new information.”

Today’s press release suggests that the global economy has slowed in response to trade disputes. In the US, business investment has been substantial, primarily driven by expenditures on Artificial Intelligence. However, consumers are cautious, and employment gains have slowed. It is nearly a certainty that the Federal Reserve will lower its overnight policy rate this afternoon.

“Growth in the euro area has moderated as US tariffs affect trade. China’s economy held up in the first half of the year, but growth appears to be softening as investment weakens. Global oil prices are close to their levels assumed in the July Monetary Policy Report (MPR). Financial conditions have continued to ease, with higher equity prices and lower bond yields. Canada’s exchange rate has been stable relative to the US dollar.”

Canada’s economy contracted in the second quarter, posting a growth rate of -1.6%. Exports fell by 27% in Q2 following a surge in exports in advance of tariffs in Q1. Business investment also fell in Q2. “In the months ahead, slow population growth and the weakness in the labour market will likely weigh on household spending.”

Employment has declined in the past two months. “Job losses have largely been concentrated in trade-sensitive sectors, while employment growth in the rest of the economy has slowed, reflecting weak hiring intentions. The unemployment rate has moved up since March, hitting 7.1% in August, and wage growth has continued to ease.”

Bottom Line

The Bank of Canada was pretty tight-lipped about future rate cuts, but given the current trajectory, we expect another rate cut when they meet again this fall. The next BoC decision date is October 29, and the central bank wraps up the year on December 10. We expect at least one more rate cut this year, ending the year with a policy rate of 2.0%-2.25%. This should help boost interest-sensitive spending, most particularly housing, where there is considerable pent-up demand.

The Bank will move cautiously, but with the Fed cutting rates again later this year, this gives the BoC cover. While some have questioned the Bank’s easing in the face of 3% core inflation, other inflation measures suggest that underlying inflation is roughly 2.5%. The economic and labour market slowdown bodes well for another rate cut.

Traders in overnight swaps continue to price in another cut from the central bank this cycle, and put the odds at about a coin flip that they’ll ease again in October.The central bank’s communications suggest that while it has resumed monetary easing to support the ailing economy, it is leery of cutting interest rates too quickly, given the potential inflation risks posed by the surge in global protectionism and tariffs.

Dr. Sherry Cooper

-

Can a 50-Year Amortization Really Fix Housing Affordability?

The housing conversation in Vancouver and Toronto has taken a fresh turn. With prices stubbornly high, the latest debate is whether extending mortgage amortizations to 50 years could make ownership more attainable. On paper, stretching payments over a longer period reduces monthly obligations, giving first-time buyers a chance to step in. But does it truly solve the affordability crisis?

Supporters highlight that aligning monthly payments with incomes offers short-term relief. A couple eyeing an $800,000 home might see their monthly payment drop by thousands if stretched over 50 years rather than 25. That breathing room could be the difference between renting indefinitely and finally buying.

Critics, however, caution against the hidden costs. A half-century loan means paying interest that could double or even triple the original principal. And the deeper issue remains untouched: limited supply and unrelenting demand keep prices high. Extending the clock doesn’t change that fundamental imbalance.

For buyers and homeowners, the question becomes less about policy experiments and more about practical solutions available today. Consider strategies like rate holds that secure current interest levels for up to 120 days, or insured mortgage products that lower down payment requirements for qualified buyers. Homeowners with existing equity can explore refinancing, creating flexibility without waiting for Ottawa to make the next move. Families are also increasingly turning to innovative tools like reverse mortgages, which allow those 55+ to unlock home equity. For example, this piece on Reverse mortgages: 55+? A cushion against the rising cost of living explains how senior homeowners are using property wealth to offset rising expenses or even support their children’s first purchase.

These are not abstract policy debates—they are actionable options that real families are already using to navigate today’s market. The conversation about 50-year amortizations reflects a shared anxiety about affordability, but the solutions may be closer than most people think.

If you’re wondering what mix of strategies might work for your situation, MorningLee.ca is a place to start exploring.

-

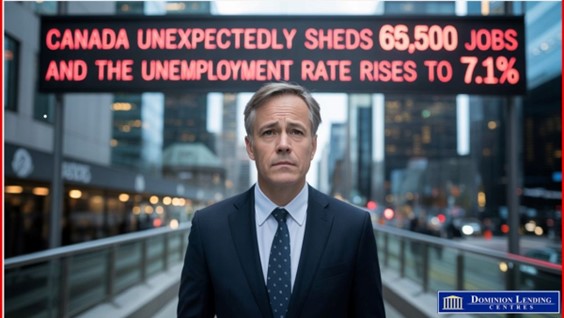

Weak August Jobs Report in Canada Bodes Well for a BoC Rate Cut

Today’s Labour Force Survey for August was weaker than expected, indicating an excess supply in the labour market and the economy. Employment fell by 66,000 (-0.3%) in August, extending the decline recorded in July (-41,000; -0.2%). The employment decrease in August was mainly due to a decline in part-time work (-60,000; -1.5%). Full-time employment was little changed in August, following a decrease in July (-51,000; -0.3%).

The employment rate—the proportion of the working-age population who are employed—fell 0.2 percentage points to 60.5% in August, the second consecutive monthly decline. The employment rate has been on a downward trend since the beginning of the year, falling 0.6 percentage points from January to August.

The number of self-employed workers fell by 43,000 (-1.6%) in August. Self-employment has trended down in recent months, offsetting gains recorded in the second half of 2024 and in early 2025.

The private sector lost 7,500 jobs last month, while the public sector shed 15,000. Regionally, the provinces of Ontario, Alberta and British Columbia led losses.

Those who were unemployed in July continued to face difficulties finding work in August. Just 15.2% of those who were unemployed in July had found work in August, lower than the corresponding proportion for the same months from 2017 to 2019 (23.3%) (not seasonally adjusted).

The participation rate—the proportion of the population aged 15 and older who were employed or looking for work—fell by 0.1 percentage points to 65.1% in August.

From May to August, the Labour Force Survey (LFS) collects labour market information from students who attended school full-time in March and who intend to return to school full-time in the fall.

The unemployment rate for returning students stood at 16.9% in August, similar to the rate observed 12 months earlier (16.3%) (not seasonally adjusted).For the summer of 2025 overall (the average from May to August), the unemployment rate for returning students aged 15 to 24 was 17.9%. This was the highest since the summer of 2009 (18.0%), excluding the pandemic year of 2020. The unemployment rate for returning students has increased each summer since 2022 (when it was 10.4%).

The unemployment rate among returning students in the summer of 2025 was higher for men (19.2%) than for women (16.8%).

Employment decreased in the professional, scientific, and technical services sector in August (-26,000; -1.3%), following five months of little change. Despite the monthly decline, employment in the industry was up 36,000 (+1.8%) compared with 12 months earlier.

Employment in transportation and warehousing fell by 23,000 (-2.1%) in August, offsetting a similar-sized increase in July. On a year-over-year basis, employment in the industry was little changed in August.

Employment change by industry in August 2025

Fewer people were working in manufacturing in August, down 19,000 (-1.0%). Compared with the recent peak of January 2025, employment in manufacturing has declined by 58,000 (-3.1%).

On the other hand, employment rose in construction (+17,000; +1.1%) in August, offsetting most of the decline in July (-22,000; -1.3%). Employment in construction has recorded little net variation since the beginning of the year, and the increase in August was the first since January.

Employment in Ontario decreased by 26,000 (-0.3%) in August. Compared to the recent peak in February 2025, employment in the province decreased by 66,000 (-0.8%) in August. The unemployment rate in Ontario declined by 0.2 percentage points to 7.7% in August, as the number of people searching for work decreased.

Since the beginning of the year, regions of Southern Ontario have faced an uncertain economic climate, brought on by the threat or imposition of tariffs, including on motor vehicle and parts exports. Across Canada’s 20 largest census metropolitan areas, the highest unemployment rates in August were in Windsor (11.1% compared with 9.1% in January), Oshawa (9.0% compared with 8.2% in January) and Toronto (8.9% compared with 8.8% in January) (three-month moving averages).

In British Columbia, employment decreased by 16,000 (-0.5%) in August, marking the second consecutive monthly decline. Losses in the month were mainly among core-aged men (-13,000; -1.2%). The unemployment rate in British Columbia rose 0.3 percentage points to 6.2%.

In Alberta, employment fell by 14,000 (-0.6%) in August, also the second consecutive monthly decrease. The most significant declines in the month were in manufacturing and in wholesale and retail trade. The unemployment rate in Alberta rose 0.6 percentage points to 8.4% in August, the highest rate since August 2017 (excluding 2020 and 2021).

Unemployment rate by province and territory, August 2025

Unemployment rates highest in southern Ontario census metropolitan areas

Employment also declined in New Brunswick (-6,500; -1.6%), Manitoba (-5,200; -0.7%), and Newfoundland and Labrador (-3,200; -1.3%) in August. Meanwhile, Prince Edward Island experienced an employment gain of 1,100 (+1.2%).

Employment held steady for a second consecutive month in Quebec in August. The number of people looking for work increased by 24,000 (+9.0%), pushing the unemployment rate up 0.5 percentage points to 6.0%.

Total hours worked were little changed in August (+0.1%) and were up 0.9% compared with 12 months earlier.

Average hourly wages among employees increased 3.2% (+$1.12 to $36.31) on a year-over-year basis in August, following growth of 3.3% in July (not seasonally adjusted).

Bottom Line

The two-year government of Canada bond yield fell about four bps on the news, while the loonie weakened. Traders in overnight swaps fully priced in a quarter-point rate cut by the Bank of Canada by year-end, and boosted the odds of a September cut to about 85%.

The Bank of Canada has made it clear that it will focus on inflation more than on increasing slack in the economy, and a September cut may still hinge on the consumer price index release, which is due a day before the rate decision.

The August US nonfarm payrolls report was also released this morning, showing that job growth stalled while the unemployment rate rose slightly to 4.3%. Several sectors, including information, financial activities, manufacturing, federal government and business services, posted outright declines in August. Job growth was concentrated in the healthcare and leisure and hospitality sectors.

Markets expect the Fed to cut rates by 25 basis points on September 17. Fed Chair Jay Powell has been under massive pressure from the White House to do so. Barring a meaningful rise in August core inflation measures, the Fed will resume cutting rates.

Dr. Sherry Cooper

-

Finding Flexibility in Today’s Real Estate Market

For many homeowners, the question isn’t whether to buy or sell—it’s whether the timing makes sense. Some buyers see opportunities in today’s housing market, but selling their current property may not feel right just yet. This is where creative financial tools come into play, offering ways to move forward without having to compromise.

Take, for example, the concept of downsizing or “right sizing.” A couple who has lived in their home for decades may want a smaller, more manageable space, or even a property in a different neighborhood. At the same time, they may not want to list their current house in today’s market. One option that provides balance is the reverse mortgage.

With a reverse mortgage, homeowners over the age of 55 can unlock a portion of their home equity without selling. This creates flexibility:

- Hold the existing property – Keep the family home while waiting for a more favorable market to sell.

- Purchase a new property with the proceeds – Use the released equity to buy a new home, without dipping into personal savings or investments.

- Choose the right time to sell – Move into the new property now, and decide later when to put the old one on the market.

- Maintain flexibility with low prepayment penalties – If circumstances change, paying off the loan early is less costly than many expect.

This approach offers a unique way to “have the best of both worlds”—living in a new space while not being pressured to sell before you’re ready. Of course, like any financial decision, there are factors to consider, such as accumulating interest over time and the eventual repayment when the home is sold. But for the right family, it can provide peace of mind and room to breathe.

To dive deeper into how reverse mortgages work in Canada and explore practical scenarios, you can read more here: Reverse mortgages: 55+? A cushion against the rising cost of living.

At the end of the day, whether you’re buying, selling, or simply planning your next step, MorningLee.ca provides knowledge and insight to help you make informed decisions.

-

Love and Hate in September

September is a polarizing month – back to school and the end of summer but also the beginning of fall and pumpkin spice everything season. And honestly, this month’s newsletter articles are polarizing too. When looking at the fall housing market, experts are polarized in their predictions on market conditions. And when it comes to a financial audit, deciding what spending mistakes you’ve been making and how to make changes might be polarizing too!

So, enjoy the articles, and here’s hoping we have more sunny days before the month races to an end.

The Fall Forecast: Cooling Temps, Hot Market Moves

Fall 2025’s real estate market theme is perhaps best summed up as “wait and see”. The spring market was flat. Experts have mixed reports about the national average home prices for the remainder of the year. Most (CREA, CMHC, etc.) predict a drop between 1.7-3.2%, but Royal LePage is an outlier still echoing their early year prediction of 3.5-5% price increase.

There are some notable regional differences. In Alberta, Saskatchewan and Quebec, they could see sales at historically high levels and faster price growth. Big Ontario and BC market declines are overshadowing these numbers and lowering the national average.

Biggest factors in the home-buying market this fall

- Affordability: the high cost of living – especially buying a home – is more than many new buyers can afford. The average MLS price for a home currently nearly $680,000. Homebuyers need big down payments, longer term loans, and will pay much more interest over the lifetime of the mortgage – none of which are appealing. Many are saying no thanks.

- US trade disputes: 49% of prospective buyers have chosen to hold off on a purchase because of impending tariffs and their ripple effects. A resolution could lead to a quick market turnaround, but there’s no way to know what’s coming.

- Economic cooling: unemployment, slower population growth and a mild recession are all contributing to a slower fall housing market.

- Rental market: Condo completions are surging, flooding the market and finally cooling off demand. People have more rental options, with potentially lower rates, which negates the need to buy. Also of note is slower household formation, meaning fewer people are looking to move out of their parents’ homes and in with their new spouse or partner.

- New builds: Builders are seeing reduced demand and cutting back production accordingly. Current tariffs are increasing the material costs for new homes, another reason to delay starts. The CMHC is predicting only 226,600 home starts for 2025.

What about rates?

The Bank of Canada has paused interest rate drops since April, which has given potential mortgagees pause. There is still one more rate cut predicted this year which could turn the market around.

Initially, the CMHC was estimating 5-year fixed rates between 5.3-5.7% this year, but with that now out the window and lower rates currently available, the remainder of 2025 is the ideal time to get a mortgage for anyone who doesn’t already have one or imminently needs to renew. With a potential Bank of Canada rate cut looming, variable rates are also still attractive.

Is anyone opting to buy this fall?

Yes! Resale homes are gaining market share, with somewhere between 464,600 and 524,600 homes expected to change hands in 2025.

There are also two main buyer demographics:

- Millennials: With remote work declining, they need to buy homes closer to their jobs. Urban market resale homes will likely be their prime targets.

- Renewals: Those needing to renew their mortgages will consider their actual needs vs their existing home. Downsizing to save costs or upsizing to accommodate changing family needs are big factors. This is the ideal time to make a move without (mortgage) penalties.

What does all this mean?

We’ll all be waiting to see what happens. If you want to buy, there is more supply and the lowest rates we’ve seen in a while. If you want to sell, the resale market is your friend. Either way, I can help you work out the mortgage you’re going to need.

Adulting 101: Back-to-School Budgeting for Real Life

If it’s time for you to stop rearranging the deck chairs on the Titanic and start a purposeful financial audit – I’ve got you. Here we’re going beyond gathering statements, categorizing expenses and hoping to reduce spending. I’m going to give you the motivation to take action by looking at the WHY, WHAT, and HOW to get you into a different mindset with better results.

Why do a financial audit?

Auditing your finances is all about identifying how you’re spending your hard-earned cash. An audit works because it uncovers money pits you didn’t realize you’d fallen in, and gets you thinking about your financial goals. An audit will:

- Identify overspending patterns

- Calculate the true cost of ownership of items like a vehicle, your home, etc.

- Catch any fraud or transaction errors

- Pinpoint areas of spending to limit or reduce

- Highlight items you’re automatically paying for but not using

- Reallocate resources to higher priority items

- Help you meet life goals that require money (like a degree, a home or the trip of a lifetime)

So, if that sounds good, it’s time to get started. What you need to ask yourself during an audit:

To get your finances on track, first get to the root of your current spending. Here’s what to ask yourself:

- What are your goals for your earnings?

- What are your life goals?

- How much do you *think* you spend vs how much do you *actually* spend on things like entertainment, shopping, and other non-essentials?

Sometimes the biggest shock of a financial audit is how different your expectations are from your reality. So let’s now figure out what you should still spend money on, and what you shouldn’t. Here’s what to ask yourself:

- What spends bring you the most joy?

- What items could you skip or cut back without much negative impact?

- What spends contribute towards your life and financial goals?

You probably can’t afford (and don’t need) everything you feel like spending money on. You’ll have to make choices. A financial audit shows your financial pitfalls and puts those spending traps into perspective against your goals.

How to stay committed:

You found a reason to conduct this financial audit, figured out what spending to cut back on, and now it’s time to action your findings. How? Step one is to set both short and mid term goals in specific time frames and reward yourself when you achieve them. SMART goals never looked better.

If it works for you, find a free app to track your card taps, and set alerts so you know immediately when you’ve gone off track. If that’s not for you, here are more strategies on how to stay committed and accountable:

- Make a visual of your goal – print a picture, make a vision board, etc.

- Share your goals with someone that will help keep you accountable

- Treat it like the first year of dating – celebrate small milestones, talk about it with your friends, and ignore the sacrifices you’re making

- Distract yourself when you’re tempted to spend – go for a walk, do a craft, get outside, make a puzzle, whatever gets you away from temptation

- Make it a game, like a week-long no-buy or going one month without eating out. You can give it a fun name like ‘dine-in December’ or ‘the week without’

- Make a direct correlation between the amount something costs and the number of hours you have to work to get it. If you earn $40/hour, and something costs $200, you’ll have to work for 5 extra hours to earn it. Is that worth while?

For the times when you’re getting derailed and need some reprieve, here’s how to make that work:

- Try to use up gift cards, store credit or points (like Optimum or Aeroplan) on the out-of-budget items

- Need more cash? Use marketplace or Kijiji to sell things you don’t need or want

Auditing your spending isn’t about guilt—it’s about gaining clarity. With a clear picture of where your money typically goes, and what you’d really like to use it for, you can make smarter choices and set yourself up for future financial success.

Economic Insights from Dr. Sherry Cooper

The Bank of Canada has maintained its target for the overnight rate at 2.75% since March 12. This was the seventh consecutive cut since mid-2024, when the Bank began lowering the rate from 5.0% in response to a potential economic slowdown caused by increased trade tensions with the United States.

Very early in the new Trump administration, tensions emerged as the president threatened to place sizable tariffs on Canadian imports not covered by the Canada-US-Mexico free trade agreement (CUSMA). President Trump has increased tariffs on non-CUSMA-compliant goods from Canada from 25% to 35%, effective August 1.

It is currently estimated that roughly 80% of Canadian exports are CUSMA-compliant, headed for 89% in the coming months. This has kept the lid on the overall tariff burden. In June, 77% of Mexican imports met the trade pact’s country of origin criteria, up from 42% May. Fitch rating service estimates the compliance proportion will rise to 83%.

In addition, there is a 50% tariff for all countries’ exports of steel and aluminum into the US. There is a 10% tariff on non-CUSMA-compliant potash, oil, and gas products. And a 50% tariff on some copper products.

Most important for Amazon shoppers, the US eliminated the de minimis treatment for low-value shipments. Goods valued at $800 or less are now

subject to all applicable duties (effective August 29).

Other tariffs are on the table. These include tariffs on Canadian lumber, which would be in addition to the existing 14.7% tariffs, as well as on Canadian dairy products. Semiconductors and pharmaceuticals are also under consideration for tariffs, though no details have been provided.

Reflective of Canadian resiliency, the Canadian services sector is holding up relatively well, but the export-heavy industries such as manufacturing and transportation are bearing the brunt of the impact.

The burning question for the Bank of Canada is how inflationary these tariffs will be. Indeed, some of the tariffs will be passed off to consumers. While theoretically tariffs lead to a one-shot uptick in prices, they don’t necessarily cause inflation—a continuous rise in the general price level.

But, as the latest data for July suggest, while headline inflation remains muted at 1.7% year-over-year, the Bank of Canada’s favoured measures of inflation average 3.05%–too high for comfort. Unless the August CPI data show a marked slowdown in core inflation, the Bank will likely retake a pass on September 17.

On the same date, traders are now signalling that the Federal Reserve will cut rates. I’m not so sure. The US economy is too resilient, and inflation is not close enough to 2.0% for Fed officials to muck around with easing. The widespread expectation that they will ease anyway in September is lifting stocks, and the actual event may cause a stock market melt-up.

The Fed left policy rates unchanged on July 30 for the fifth consecutive confab over the past seven months. The statement’s economic assessment

was slightly more downbeat, in line with the data on the ground. The risk assessment didn’t refer to uncertainty as having “diminished”, with the August 1 tariff announcements looming. And, Governors Bowman and Waller dissented in favour of a quarter-point rate cut. The vote was 9-to-2, with Governor Kugler absent and not voting. (Two days later, Kugler announced her resignation.) In the press conference, Chair Powell said: “We see our current policy stance as appropriate to guard against inflation risks. We are also attentive to risks on the employment side of our mandate.

Another key determinant of central bank policy is the strength of economic growth, as reflected in the employment data–a far timelier indicator than the GDP data. For example, while we still haven’t seen the number for second-quarter GDP growth in Canada, we have monthly employment data through the end of July.

This and other leading indicators, such as the stock market, suggest that the slowdown in economic activity has been more moderate than many feared. The layoffs are growing in the hardest-hit sectors—steel, aluminum, autos and parts—the jobless rate for July was steady at 6.9%.

So, the BoC is likely to have another ‘wait and see’ meeting. But the one sector that has declined significantly in the past year is housing. This provides a golden opportunity, especially for first-time and move-up buyers.

Home prices have fallen, and in many regions (GTA and GVA), sellers are motivated. Supply has increased sharply, and multiple-bidding situations are rare.

All potential buyers should be out there looking for bargains because

everything is on sale (as well as for sale). Finally, mortgage rates are low—yes, low.

We will not see a return to two-handle mortgage rates, barring another global pandemic. And, even then, the central banks would know better than to take rates down so much, for so long.

The July data showed an uptrend in housing activity. We are likely looking towards a relatively strong Fall marketing season.