Refinancing Experts | Residential & Commercial Mortgage Solutions | Morning Lee

Expert refinancing solutions for homeowners and businesses. Lower rates, access equity, and consolidate debt. Get personalized refinancing strategies today.

Unlock Your Property’s Financial Potential Through Strategic Refinancing

What Is Refinancing?

Refinancing replaces your existing mortgage with a new loan, typically to:

- Secure lower interest rates

- Access home/property equity

- Consolidate high-interest debt

- Change loan terms (amortization period)

- Switch from variable to fixed rates (or vice versa)

Real Example: Commercial landlord accessed $1.2M equity to acquire adjacent property through refinancing

Why Consider Refinancing?

Residential Benefits

- Rate Reduction: Save 0.5-2.5% on current market rates

- Debt Consolidation: Combine credit cards/loans into lower-interest mortgage

- Renovation Funding: Access up to 80% of current home equity

- Mortgage Optimization: Adjust amortization for cash flow needs

Commercial Advantages

- Portfolio Restructuring: Consolidate multiple properties into single loan

- Value-Add Capital: Fund renovations to increase NOI

- Cash Flow Relief: Extend amortization periods

- Bridge Financing: Secure funds for new acquisitions

Our Process

*4-Step Framework for Optimal Results*

- Equity & Savings Analysis

- Current valuation assessment

- Break penalty calculation

- Rate comparison across lenders

- Solution Architecture

- Debt consolidation planning

- Cash-out refinancing structuring

- Term optimization strategy

- Lender Negotiation

- Rate discount securing

- Fee waivers (appraisal, legal)

- Covenant flexibility

- Seamless Transition

- Legal coordination

- Payout management

- Post-refinance rate monitoring

Why Choose Morning Lee for Refinancing?

Rate Reduction Mastery

Equity Access Expertise

- Residential: Up to 100% loan-to-value

- Commercial: Up to 100% LTV loan to value

- Portfolio: Cross-collateralization strategies

Break Cost Mitigation

- High success rate in penalty negotiation/reduction

- Blended rate solutions

- Portability strategies

Specialized Solutions

- Commercial:

- NOI improvement refinancing

- Zoning change value capture

- Anchor tenant lease leveraging

- Residential:

- Credit repair refinancing

- Rental property cash flow optimization

- Construction draw management

When Refinancing Makes Strategic Sense

| Scenario | Residential Solution | Commercial Solution |

|---|---|---|

| Rates Drop 0.75%+ | Rate term reduction | Interest cost arbitrage |

| Property Value Rises | Equity access for renovations | Portfolio expansion capital |

| Credit Score Improves | Prime rate qualification | Covenant requirement reduction |

| Business Needs Change | N/A | Equipment financing roll-in |

Start Your Equity Taking Out Journey

Step 1: Savings Assessment

Calculate Your Refinancing Savings

Step 2: Strategy Session

Book 15-min Refinancing Audit

Step 3: Application Process

*”We’ve optimized many people through strategic refinancing – let our expertise unlock your property’s financial potential.”*

— Mortgage Expert – Morning Lee

-

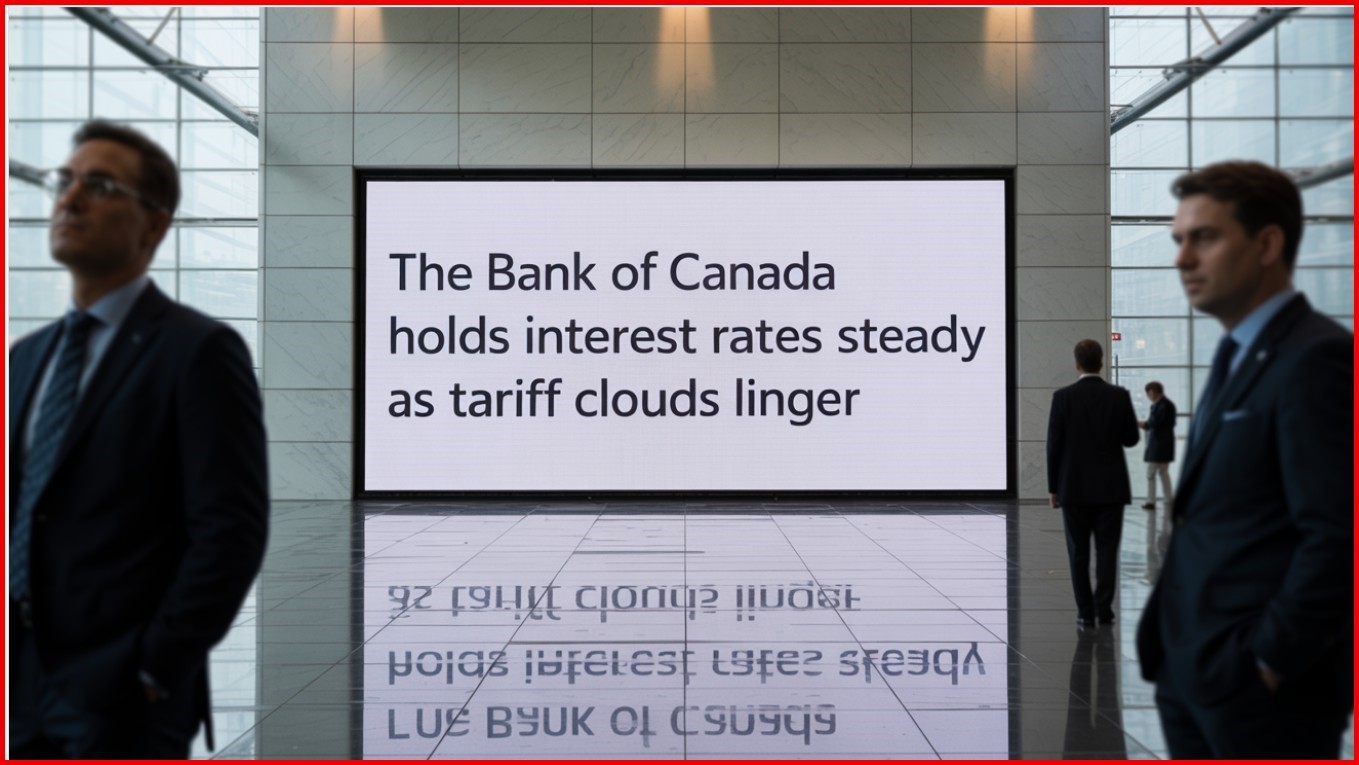

Bank of Canada Holds Rates Steady As Tariff Turmoil Continues

Bank of Canada Holds Rates Steady As Tariff Turmoil Continues As expected, the Bank of Canada held its benchmark interest rate unchanged at 2.75% at today’s meeting, the third consecutive rate hold since the Bank cut overnight rates seven times in the past year. The Governing Council noted that the unpredictability of the magnitude and duration of tariffs posed downside risks to growth and lifted inflation expectations, warranting caution regarding the continuation of monetary easing.

Trade negotiations between Canada and the United States are ongoing, and US trade policy remains unpredictable.

While US tariffs are disrupting trade, Canada’s economy is showing some resilience so far. Several surveys suggest consumer and business sentiment is still low, but has improved. In the labour market, we are seeing job losses in the sectors that rely on US trade, but employment is growing in other parts of the economy. The unemployment rate has moved up modestly to 6.9%.

Inflation is close to the BoC’s 2% target, but evidence of underlying inflation pressures continues. “CPI inflation has been pulled down by the elimination of the carbon tax and is just below 2%. However, a range of indicators suggests underlying inflation has increased from around 2% in the second half of last year to roughly 2½% more recently. This largely reflects an increase in prices for goods other than energy. Shelter cost inflation remains the biggest contributor to CPI inflation, but it continues to ease. Surveys indicate businesses’ inflation expectations have fallen back after rising in the first quarter, while consumers’ expectations have not come down”.

The Bank asserted today that there are reasons to think that the recent increase in underlying inflation will gradually unwind. The Canadian dollar has appreciated, which reduces import costs. Growth in unit labour costs has moderated, and the economy is in excess supply. At the same time, tariffs impose new direct costs, which will be gradually passed through to consumers. In the current tariff scenario, upside and downside pressures roughly balance out, so inflation remains close to 2%.

The central bank provided alternative scenarios for the economic outlook. In the de-escalation scenario, lower tariffs improve growth and reduce the direct cost pressures on inflation. In the escalation scenario, higher tariffs weaken the economy and increase direct cost pressures.

So far, the global economic consequences of US trade policy have been less severe than feared. US tariffs have disrupted trade in significant economies, and this is slowing global growth, but by less than many anticipated. While growth in the US economy looks to be moderating, the labour market has remained solid. And in China, lower exports to the United States have largely been replaced with stronger exports to other countries.

In Canada, we experienced robust growth in the first quarter of 2025, primarily due to firms rushing to get ahead of tariffs. In the second quarter, the economy looks to have contracted, as exports to the United States fell sharply—both as payback for the pull-forward and because tariffs are dampening US demand.

The gap between the 2.75% overnight policy rate in Canada and the 4.25-4.50% policy rate in the US is historically wide. Another cause of uncertainty is the fiscal response to today’s economic challenges. The One Big Beautiful Bill has passed, and it will add roughly US$4 trillion to the already burgeoning US federal government’s red ink. This has caused a year-to-date rise in longer-term bond yields, steepening the yield curve.

The slowdown of the housing sector since Trump’s inauguration has been a substantial drain on the economy. The Monetary Policy Report (MPR) for July states that “growth in residential investment strengthens in the second half of 2025, partially due to an increase in resale activity after the steep decline in the first half of the year. Growth in residential investment is moderate over 2026 and 2027, supported by dissipating trade uncertainty and rising household incomes.”

Bottom Line

We expect the Canadian economy to post a small negative reading (-0.8%) in Q2 and (-0.3%) in Q3, bringing growth for the year to 1.2%. The next Governing Council decision date is September 17, which will give the Bank time to assess the underlying momentum in inflation and the dampening effect of tariffs on economic activity.

If inflation slows over the next couple of months and the economy slows in Q2 and Q3 as widely expected, the Bank will likely cut rates one more time this year, bringing the overnight rate down to 2.50%, within the neutral range for monetary policy. Bay Street economists have varying views on the rate outlook (see chart above). While the Fed will hold rates steady today, despite the incredible pressure coming from the White House, the Bank of Canada could well cut rates one more time this year.Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres -

How a Vancouver Mortgage Broker Residential Specialist Can Help with Non-Traditional Down Payments

When trying to secure a home loan, most people assume the rules are set in stone: stable job, great credit, and a conventional down payment coming straight from your savings. But for many buyers in the Vancouver market, life just doesn’t work that cleanly. That’s where a Vancouver Mortgage Broker Residential professional comes in—someone who understands how to work with non-traditional down payments and align your situation with lenders that are flexible enough to say “yes.”

Vancouver Mortgage Broker Residential Insight: What Counts as a Non-Traditional Down Payment

The most widely accepted form of a down payment is your own personal savings, typically seasoned in a bank account for 90 days or more. But what happens if your down payment source doesn’t fit that mold?

Here are a few common examples of non-traditional down payments:

- Gifted funds from family

- Borrowed funds (secured or unsecured)

- Proceeds from selling assets (e.g., vehicle, cryptocurrency, overseas property)

- Business income lump sums or irregular commissions

- RRSP withdrawals under the First-Time Home Buyer’s Plan (FTHBP)

While some lenders—particularly the big five A-lenders—may flag these as unverifiable or unstable, alternative lenders and B-lenders may still be willing to work with you.

According to Canada Mortgage and Housing Corporation (CMHC) guidelines, gifted down payments must come with a signed letter and proof that the gift is non-repayable. However, not every lender interprets CMHC’s rules the same way. A Vancouver Mortgage Broker Residential expert can help match your scenario with lenders who accept these sources with fewer obstacles.

How a Vancouver Mortgage Broker Residential Expert Navigates Lender Rules for Non-Traditional Down Payments

Banks are risk-averse by design. They want your down payment to show long-term savings habits and financial discipline. In contrast, B-lenders and private lenders look at your overall risk profile more holistically:

- Is your credit score acceptable (even if not perfect)?

- Do you have a stable source of income, even if self-employed?

- Is your debt service ratio within manageable levels?

As noted in a recent market report from Today’s Report Shows Inflation Remains a Concern, Forestalling BoC Action, rising inflation and stalled Bank of Canada decisions are creating tighter conditions—but also more opportunity for flexible financing solutions, especially in non-traditional arrangements.

Top Reasons to Work with a Vancouver Mortgage Broker Residential Specialist

A Vancouver Mortgage Broker Residential advisor brings more than just connections—they bring insight into which lenders tolerate what, and how to properly document your down payment to avoid delays or denials.

1. Navigating B-Lender and Private Mortgage Options

A mortgage broker can help package your non-traditional down payment in a way that meets the documentation requirements of a B-lender or private institution. This might include:

- Drafting a gift letter correctly

- Explaining irregular deposits from a business

- Structuring short-term loans from family or friends

Each lender has their own checklist—brokers know how to meet them without triggering unnecessary red flags.

2. Reducing Rejection Risk by Pre-Vetting Your Scenario

Many buyers don’t realize they can get pre-assessed for lender fit before submitting a formal application. This helps avoid hard credit checks and mortgage declines that stay on your record for months.

If you’ve already been turned down once, a broker can also re-strategize the timing and submission of your new application. Timing matters. For example, if you’re self-employed and expecting a stronger annual income report, delaying the submission could improve your approval odds.

3. Structuring Co-Applications for Maximum Impact

Using a co-signer or spouse’s income can be a game-changer. A mortgage broker can guide you on how to present shared income without muddying the waters of liability. This is especially useful if your down payment is unconventional but your household income is stable.

Why Compliance Matters: A Vancouver Mortgage Broker Residential Perspective

It’s not enough to find a lender who might accept your situation—you also need to comply with federal regulations, such as anti-money laundering (AML) rules. This is where mortgage brokers play a crucial legal role: making sure your transaction is both feasible and compliant.

Every deposit and every transfer needs a paper trail. A good Vancouver Mortgage Broker Residential partner will ensure you stay onside, especially when using funds from abroad or sources like crypto wallets and equity sales.

Beyond Mortgages: Why Vancouver Mortgage Broker Residential Clients Need Property Risk Assessments

Finding a lender is one thing—finding a safe property is another. Many deals fall through because buyers overlook title issues, zoning problems, or hidden structural risks. Before you invest, consider running a background check on the property with EstateDetect.com—a real estate detective service that investigates potential red flags before you commit. It’s one more way to safeguard your deal from surprise issues.

Final Thoughts

Getting a mortgage with a non-traditional down payment might feel like threading a needle—but with the right support, it’s absolutely doable. A knowledgeable Vancouver Mortgage Broker Residential expert can map out your options, prepare your documents, and link you with lenders that see the full picture—not just the fine print.

To explore your options or find out if your down payment qualifies, visit MorningLee.ca and start your financing journey with a broker who actually listens.

-

How to Buy Residential Property in Vancouver When Your Down Payment Falls Short

For many first-time homebuyers, the dream to buy residential property in Vancouver can feel just out of reach—especially when it comes to saving up enough for a down payment. With Vancouver’s competitive residential real estate market and rising prices, even a modest home can require a sizable upfront investment. But here’s the good news: falling short on your down payment doesn’t always mean putting your homeownership plans on hold. Let’s explore three proven solutions that may help you get into your new home sooner than you think.

1. Understanding Down Payment Tiers When You Buy Residential Property in Vancouver

Canada’s down payment structure depends on many factors:

- the downpayment can be as low as 5%, even 0% for some cases. Yes, you are not wrong, it is Zero.

- Even one or a few banks said NO, may other banks will say yes. There hundreds, thousands banks in Canada and USA.

Finding the right bank and right program among so many of them is super important. About this, a mortgage broker is the best choice for you.

2. Use Government Assistance When Buying Residential Property in Vancouver

There are many assisting programs and special programs by governments, especially for young people, first-time home buyers, special situations.

For example, the First-Time Home Buyer Incentive (FTHBI) might be an option. This federal program allows eligible buyers to borrow 5% or 10% of the home’s purchase price to put toward the down payment. The incentive is repayable, interest-free, and designed to make monthly mortgage payments more manageable.

For details, please check out the government information here

If you want to get more and updates about this kind of information, please register our newsletter to receive related news, updates, polices, etc.

3. Using Gifted Down Payments to Buy Residential Property in Vancouver — What’s Legal and What’s Not

Another common method for buyers in Vancouver is receiving gifted down payments from close family. Most Canadian lenders accept this form of funding—provided there’s clear documentation that it is indeed a gift, not a loan.

Your lender will typically require:

- A signed gift letter from the family member.

- Proof the funds are in your account before closing.

- In some cases, a paper trail showing how the funds moved.

Remember, the source of your down payment is heavily scrutinized by lenders and underwriters. Legal transparency is key.

Buy Residential Property in Vancouver Using Non-Traditional Down Payment Sources

In today’s market, many buyers rely on the guidance of a mortgage broker to access lenders who accept non-traditional down payment sources, such as borrowed funds against other assets or cash flow from side businesses. Not all banks will work with these types of arrangements—but alternative lenders and B-lenders often will, especially with the right documentation and a solid income history.

This is where professionals like those at MorningLee.ca come in. With experience in both real estate and financing, they can connect you with lenders who look beyond just the big five banks.

Bonus Tip: Don’t Skip the Property Check

If you’re stretching your finances to secure a home, the last thing you want is a surprise repair bill. Before you buy, consider using tools like EstateDetect.com — a platform that helps homebuyers investigate property risks and hidden issues, giving you peace of mind and negotiation power.

The Market is Stabilizing — Act While Conditions Are Right

As home sales rise and prices begin to stabilize, Vancouver’s real estate market is entering a window of opportunity. Acting now—with the right financial strategy—can make all the difference.

And if you’re ready to take the next step, MorningLee.ca is here to help guide you through both the buying and financing process—professionally, efficiently, and with your best interest in mind.

-

Today’s Report Shows Inflation Remains a Concern, Forestalling BoC Action

Canadian consumer prices accelerated for the first time in four months in June, and underlying price pressures firmed, likely keeping the central bank from cutting interest rates later this month.

The annual inflation rate in Canada rose to 1.9% in June from 1.7% in May, aligning with market expectations. Despite the pickup, the rate remained below the Bank of Canada’s mid-point target of 2% for the third consecutive month.

Headline inflation grew at a faster pace, as gasoline prices fell to a lesser extent in June (-13.4%) than in May (-15.5%). Additionally, faster price growth for some durable goods, such as passenger vehicles and furniture, put upward pressure on the CPI in June.

Prices for food purchased from stores rose 2.8% year-over-year in June, following a 3.3% increase in May.

Year over year, the CPI excluding energy (+2.7%) remained higher than the CPI in June, partly due to the removal of consumer carbon pricing in April.

Monthly, the CPI rose 0.1% in June. On a seasonally adjusted monthly basis, the CPI was up 0.2%.

The Bank of Canada’s two preferred core inflation measures accelerated slightly, averaging 3.05%, up from 3% in May, and above economists’ median projection. The three-month moving annualized average of the core rates surged to 3.39%, from 3.01% previously.

There’s also another important sign of firmer price pressures: The share of components in the consumer price index basket that are rising by 3% or more — another key metric the central bank’s policymakers are watching closely — expanded to 39.1%, from 37.3% in May.

Bottom Line

The chart below, created by our friends at Mortgage Logic News, shows that Canadian economic data have come in stronger than expected on average in recent weeks. This was evident in the June employment report. As a result, the Bank of Canada is likely to remain on the sidelines on July 30 for the third consecutive meeting. The Canadian economy appears to be weathering the tariff storm better than expected, at least for now.

While we expect to see a negative print on Q2 GDP growth, a bounce back to positive growth in Q3 is also possible, precluding the much-expected Canadian recession.

The June inflation data, released today for the US, was weaker than expected for the core price index. Declines in car prices helped mitigate tariff-related increases in other goods within the US consumer basket.

The US inflation data could draw even greater calls from President Trump for the Federal Reserve to lower interest rates. While some officials have expressed a willingness to cut rates when the central bank meets in two weeks, policymakers are generally still divided as to whether tariffs will cause a one-time price shock or something more persistent. They will leave rates unchanged for now.

Dr. Sherry Cooper