Buying Property in Vancouver Residential – Vancouver Best Realtor – Morning Lee

Buying property in Vancouver is not an easy job, but I can make it easier for you. We have three different program options tailored for different people. I believe one of them will be a good fit for you.

Self Service Buyer Program

Services include the followings

- First Time Consulting

- Open House Showing

- Arranging Private Showing

- General Consulting

- Offer Strategy Consulting

- Writing an offer

- Negotiating and Accepted Offer

- Subjects Consulting and Subjects removal

- Completion Consulting

- Possession Consulting

Requirement for you

- You can arrange your own travelling to open houses and showings

- Familiar with internet

- Know local laws very well

- Know real estate market very well

- Know the community very well

- Funds are ready or will be ready

Benefit For You

- Cash Bonus, buyer rebate, To You after Closing

Semi-Self Service Program

Services include the followings

- First Time Consulting

- Open House Showing

- Arranging Private Showing

- General Consulting

- Offer Strategy Consulting

- Writing an offer

- Negotiating and Accepted Offer

- Subjects Consulting and subjects removal

- Completion Consulting

- Possession Consulting

Requirement for you

- You can arrange your own travelling to open houses and showings

- Familiar with internet

- Know local laws very well

- Know real estate market very well

- Know the community very well

- Funds are ready or will be ready

Benefit For You

- Cash Bonus, buyer rebate, To You after Closing

Full Service Buyer Program

Services include the followings

- First Time Consulting

- Open House Showing

- Arranging Private Showing

- General Consulting

- Offer Strategy Consulting

- Writing an offer

- Negotiating and accepted offer

- Subjects Consulting and subjects removal

- Completion Consulting

- Possession Consulting

Requirement For You

- Funds are ready or will be ready

Benefit For You

- Full service for purchasing your dream home

This option is a traditional classic service. But most people don’t need all the services. Which is why we offer other options.

Self-Service Buyer Program for Buying Property in Vancouver

Buying Property in Vancouver is a very simple and easy job for some experienced and skilled people – for example, real estate investors, former Realtors, or those who have experiences buying properties in Vancouver, or those who own multiple properties. For these people, we offer only essential services, saving time for you and us. This way, you will receive a large cash bonus, buyer rebate, after closing, which comes from our buyer agent commission.

However, please note that some listing agents set conditions regarding the buyer agent’s commission. For example, if the buyer agent does not attend an open house or private showing, the commission may be reduced significantly—sometimes to as low as $500.

In such cases, either you must avoid those listings, or there will be no cash bonus (buyer rebate) available to you

For more information about our Self-Service Buyer Program, please contact us directly. contact us.

Semi-Self Service Buyer Program for Buying Property in Vancouver

Some buyers don’t need full service but may not feel entirely comfortable with the self-service buyer program. For those clients, we provide essential services along with a few additional supports. This approach still saves time, which is why you can also receive a cash bonus (buyer rebate).

That said, please understand the same limitations apply: some listing agents require the buyer agent’s presence at showings or open houses. If those conditions are not met, the buyer agent’s commission may be reduced to a small amount, such as $500. In those cases, either avoid such listings, or a rebate cannot be provided.

For more information about our Semi-Self-Service Buyer Program, please contact us directly. contact us.

Full Service Buyer Program for Buying Property in Vancouver

As the name suggests, the Full-Service Buyer Program includes all services typically provided by a buyer’s agent. This is especially suitable for newcomers or anyone who may not feel confident navigating the self-service or semi-self-service programs.

With this option, we handle everything for you—making the home-buying process as smooth and stress-free as possible.

For more information about our Full Service Buyer Program, please contact us directly. contact us.

If you need mortgage, please contact us for our mortgage servcie

Another website built by WealthDao Consulting. For E-Commerce Consulting, Digital Marketing Consulting, Profit Consulting, please visit WealthDao Consulting

-

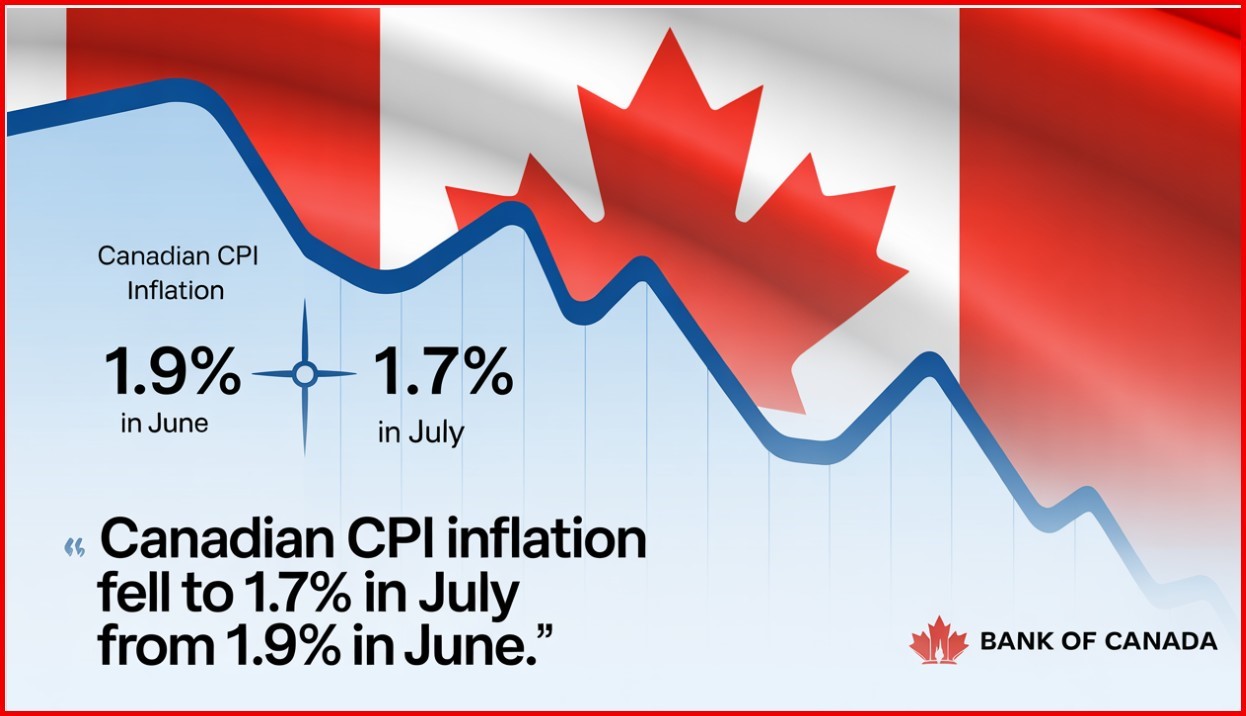

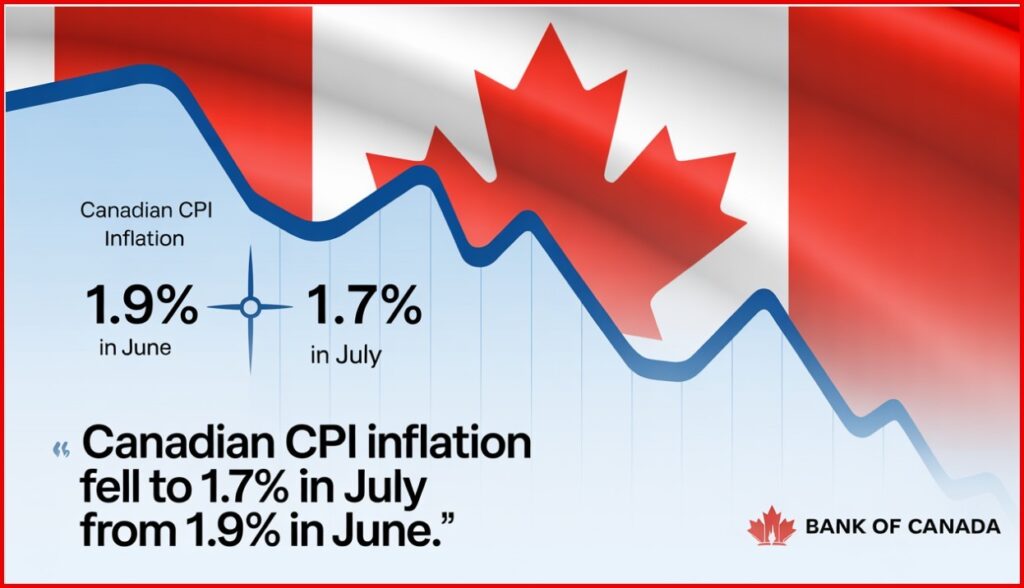

CPI Report Shows Headline Inflation Cooling, But Core Inflation Remains Troubling

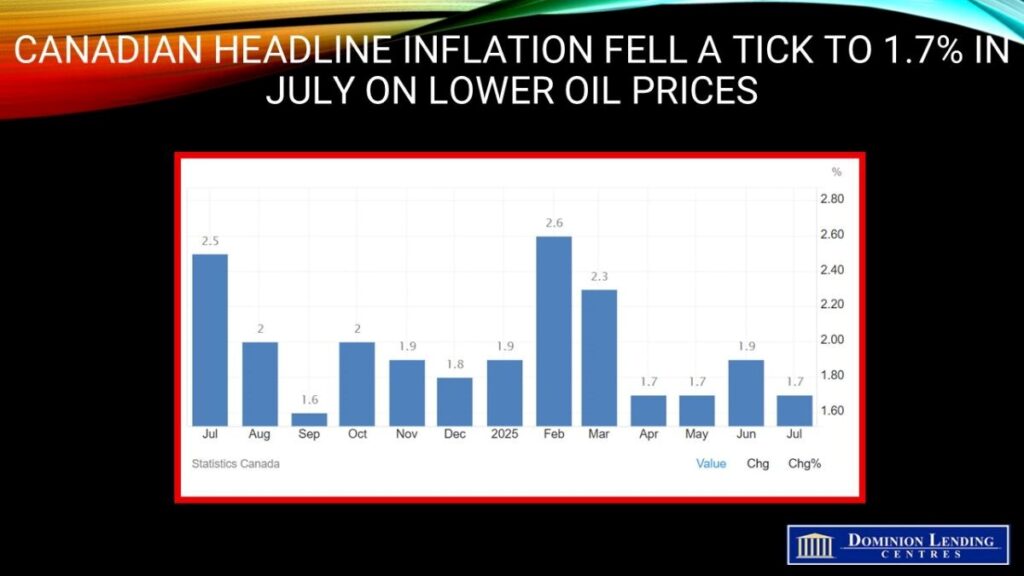

Canadian consumer prices decelerated to 1.7% y/y in July, a bit better than expected and down two ticks from June’s reading.

Gasoline prices led the slowdown in the all-items CPI, falling 16.1% year over year in July, following a 13.4% decline in June. Excluding gasoline, the CPI rose 2.5% in July, matching the increases in May and June.Gasoline prices fell 0.7% m/m in July. Lower crude oil prices, following the ceasefire between Iran and Israel, contributed to the decline. In addition, increased supply from the Organization of the Petroleum Exporting Countries and its partners (OPEC+) put downward pressure on the index.

Moderating the deceleration in July were higher prices for groceries and a smaller year-over-year decline in natural gas prices compared with June.

The CPI rose 0.3% month over month in July. On a seasonally adjusted monthly basis, the CPI was up 0.1%.

In July, prices for shelter rose 3.0% year over year, following a 2.9% increase in June, with upward pressure mostly coming from the natural gas and rent indexes. This was the first acceleration in shelter prices since February 2024.

Prices for natural gas fell to a lesser extent in July (-7.3%) compared with June (-14.1%). The smaller decline was mainly due to higher prices in Ontario, which increased 1.8% in July after a 14.0% decline in June.

Rent prices rose at a faster pace year over year, up 5.1% in July following a 4.7% increase in June. Rent price growth accelerated the most in Prince Edward Island (+5.6%), Newfoundland and Labrador (+7.8%) and British Columbia (+4.8%).

Moderating the acceleration in shelter was continued slower price growth in mortgage interest cost, which rose 4.8% year over year in July, after a 5.6% gain in June. The mortgage interest cost index has decelerated on a year-over-year basis since September 2023.

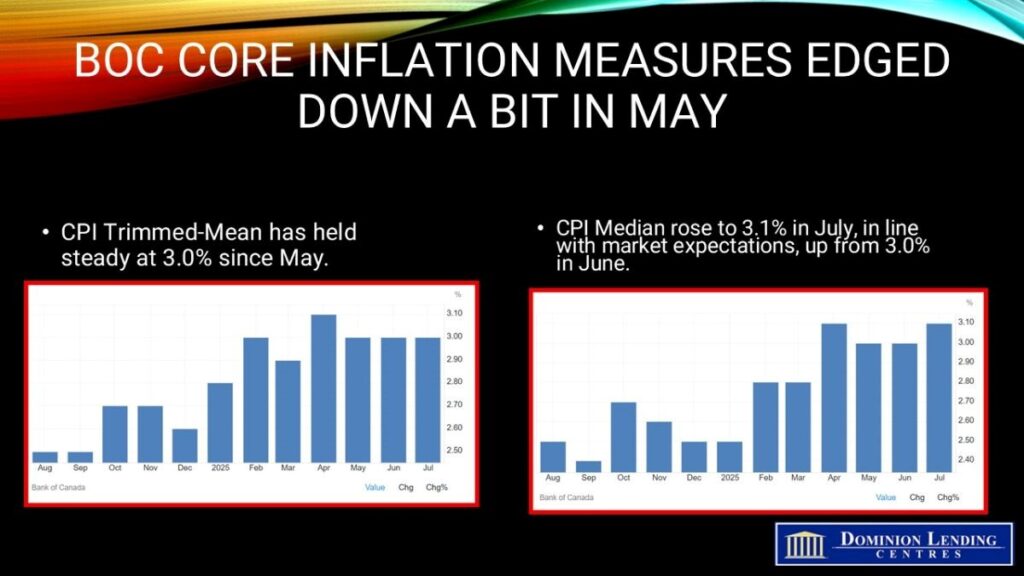

The Bank of Canada’s two preferred core inflation measures accelerated slightly, averaging 3.05%, up from 3% in May, and above economists’ median projection. Traders see the continued strength in core inflation as indicative of relatively robust household spending.

There’s also another critical sign of firmer price pressures: The share of components in the consumer price index basket that are rising by 3% or more — another key metric the central bank’s policymakers are watching closely — expanded to 40%, from 39.1% in June.

CPI excluding taxes eased to 2.3%, while CPI excluding shelter slowed to 1.2%. CPI excluding food and energy dropped to 2.5%, and CPI excluding eight volatile components and indirect taxes fell to 2.6%.

The breadth of inflation is also rising. The share of components with the consumer price index basket that are increasing 3% and higher — another key metric that the bank’s policymakers are following closely — fell to 37.3%, from 39.1% in June.

Bottom Line

With today’s CPI painting a mixed picture, the following inflation report becomes more critical for the Governing Council. The August CPI will be released the day before the September 17 meeting of the central bank. There is also another employment report released on September 5.

Traders see roughly 84% odds of a Federal Reserve rate cut when they meet again on Sept 17–the same day as Canada. Currently, the odds of a rate cut by the BoC stand at 34%. Unless the August inflation report shows an improvement in core inflation, the Bank will remain on the sidelines.

Dr. Sherry Cooper -

Today’s Lowest Rates Up and Down at The Same Time

The 3-year fixed rate has hit a new low at 3.69%, but the 5-year lowest fixed rate has gone up. The upward and downward pressures are still fiercely competing.

If you are considering a loan in the near future, you need to pay close attention to rate changes and seize the timing to lock in a contract that is favourable to you.

If your current rate is relatively high, 5% or even over 6%, you need to carefully calculate and compare: the penalty for breaking your current contract versus the money saved by switching to a lower rate — which one is more cost-effective. An extra surprise may even make you scream!

Even banks say no, for low income, low credit, low down pay, Morning will find a way, for you.

-

Owning $10 million in real estate but denied a loan—how to turn rejection into a powerful tool

Imagine Investor A, holding seven properties with a total value $10+ million. They spot a rare opportunity: sellers urgently offloading prime real estate at below-market price. But when they approach traditional banks for a loan, they hit a wall.

The Dilemma

Despite looking like a financial winner, reality bites:- Self-employment income nearly zero due to market changes

- Loans only $2 million, net assets $8 million

- Primary residence worth $2.2 million, mortgage $200k

- Rental income covers mortgage with positive cash flow, but after daily expenses and maintenance, disposable cash is limited

- Excellent credit score and history

Yet, major banks refused their applications. Why? Income too low, debt too high, and unable to pass standard stress tests.

Breaking the Gridlock

Investor A came to us, and we break it through by thinking differently. While banks focus on regular income, we realized Investor A’s wealth was “locked in walls.” Six solutions emerged by us:1. Reverse Mortgage (Primary Residence, Age 55+)

- Benefits:

- No income verification.

- Flexible credit requirements.

- No down payment required.

- Access up to ~50% of your home equity.

- Funds received as monthly payments, lump sum, or instalments.

- Minimal fees, almost none.

- Fast approval.

- Drawbacks:

- Only available for primary residences (not investment properties).

- Maximum Cash Available: ~$1 million

2. “Enhanced” Reverse Mortgage (Primary Residence, No Age Requirement)

- Benefits:

- No age requirement.

- No income verification.

- Flexible credit requirements.

- No down payment required.

- Access up to 60% of your home equity.

- Funds received as monthly payments, lump sum, or instalments.

- Fast approval.

- Cancel anytime without penalty.

- Drawbacks:

- Only available for primary residences (not investment properties).

- Higher fees.

- Maximum Cash Available: ~$1.2 million

3. First Mortgage Home Equity Line of Credit

- Benefits:

- Access up to 75% of home equity.

- No income verification.

- No age requirement.

- Flexible credit requirements.

- Pay interest only on amounts drawn; no payment if unused. Access funds freely and flexibly.

- Drawbacks:

- Higher fees.

- Requires terminating existing first mortgage.

- Maximum Cash Available: ~$6 million

4. First Mortgage Home Equity Mortgage

- Benefits:

- Access up to 75% of home equity.

- No income verification.

- No age requirement.

- Flexible credit requirements.

- Lower fees than a First Mortgage HELOC.

- Drawbacks:

- Requires terminating existing first mortgage.

- Monthly payments required.

- Maximum Cash Available: ~$6 million

5. Second Mortgage Home Equity Line of Credit

- Benefits:

- No income verification.

- No age requirement.

- Flexible credit requirements.

- Access up to 75% of home equity.

- Pay interest only on amounts drawn; no payment if unused. Access funds freely and flexibly.

- Does not require terminating existing first mortgage.

- Drawbacks:

- Higher fees.

- Maximum Cash Available: ~$6 million

6. Second Mortgage Home Equity Loan

- Benefits:

- No income verification.

- No age requirement.

- Flexible credit requirements.

- Access up to 75% of home equity.

- Does not require terminating your existing first mortgage.

- Lower fees than a Second Mortgage HELOC.

- Drawbacks:

- Monthly payments required.

- Maximum Cash Available: ~$6 million

Investor A opted for a mix of all six, leveraging each solution’s strengths while minimizing drawbacks according to the banks policies and his own situation like title, balance, interest rate, etc .

The Result

Investor A secured a $5 million credit line with two remarkable features:- Off loaded the cash pressure— and interest applies only when money is used

- Ready to close good deals any time and immediate access to funds when needed – won’t miss any good opportunities to build up more wealth.

From nearly depleted cash reserves, Investor A now had millions ready to seize undervalued properties, paying cash instantly. No income verification, no stress tests, no mandatory monthly payments—like turning their property into a giant credit card that only charges when used.

Practical Impact

Opportunities came faster than expected. Sellers in a slow market offered below-market prices with room to negotiate. While others waited for bank approvals, Investor A could pay in cash, creating a competitive edge. The secret wasn’t having money—it was unlocking dormant assets to capitalize on timing and market gaps.Key Takeaway

Banks have rules, but asset value is undeniable. When income-based paths fail, check the “walls” you’ve built—every brick could be emergency cash or a lever to unlock opportunities. Investor A’s transformation? From chasing bank loans to letting assets speak for themselves.Assess your own available funds immediately: Evaluate available credit limit.

For buyers, sellers, or anyone navigating property financing, understanding alternative funding strategies can make the difference between watching opportunities slip away or seizing them confidently.

Explore more insights and strategic approaches at MorningLee.ca:Case Study: How Debt Restructuring Can Save You Thousands

For a safer, smarter property purchase, conduct real estate due diligence for comprehensive property inspections and risk assessments.

-

Canadian Homebuyers Return in July, Posting the Fourth Consecutive Sales Gain

Today’s release of the July housing data by the Canadian Real Estate Association (CREA) showed good news on the housing front. Following a disappointing spring selling season, National home sales were up 3.8% in July from the month before, with Toronto seeing transactions rebound 35.5% since March. However, the total number of Toronto sales remains low by historical standards.

On a year-over-year basis, total transactions have risen 11.2% since March.

There is growing confidence that the Canadian economy will resiliently weather the tariff trauma. The Canadian dollar is up, and longer-term interest rates have edged downward in the past ten days. Traders are now anticipating a rate cut by the Federal Reserve in September.

Tuesday’s release of the Canadian CPI will provide another data point for the Bank of Canada. Economic growth has held up, in large part because much of the pain from tariffs has been confined to industries singled out for levies, including autos, steel and aluminum.

Shaun Cathcart, the real estate board’s senior economist, said, “With sales posting a fourth consecutive increase in July, and almost 4% at that, the long-anticipated post-inflation crisis pickup in housing seems to have finally arrived. The shock and maybe the dread that we felt back in February, March and April seem to have faded,” as people become less concerned about their future employment.

New Listings

New supply was little changed (+0.1%) month-over-month in July. Combined with the notable increase in sales, the national sales-to-new listings ratio rose to 52%, up from 50.1% in June and 47.4% in May. The long-term average for the national sales-to-new listings ratio is 54.9%, with readings roughly between 45% and 65% generally consistent with balanced housing market conditions.

There were 202,500 properties listed for sale on all Canadian MLS® Systems at the end of July 2025, up 10.1% from a year earlier and in line with the long-term average for that time of the year.

“Activity continues to pick up through the transition from the spring to the summer market, which is the opposite of a normal year, but this has not been a normal year,” said Valérie Paquin, CREA Chair. “Typically, we see a burst of new listings right at the beginning of September to kick off the fall market, but it seems like buyers are increasingly returning to the market.

There were 4.4 months of inventory on a national basis at the end of July 2025, dropping further below the long-term average of five months of inventory as sales continue to pick up. Based on one standard deviation above and below that long-term average, a seller’s market would be below 3.6 months, and a buyer’s market would be above 6.4 months.

Home Prices

The National Composite MLS® Home Price Index (HPI) was unchanged between June and July 2025. Following declines in the first quarter of the year, the national benchmark price has remained mostly stable since May.

The non-seasonally adjusted National Composite MLS® HPI was down 3.4% compared to July 2024. This was a smaller decrease than the one recorded in June.

Based on the extent to which prices fell off in the second half of 2024, look for year-over-year declines to continue to shrink in the months ahead.

Bottom Line

Homebuyers are responding to improving fundamentals in the Canadian housing market. Supply has risen as new listings surged until May of this year. Additionally, the benchmark price was $688,700, 3.4% lower than a year earlier. That decrease was smaller than in June, and the board expects year-over-year declines to continue shrinking, it said in a statement.While many expect the Fed to ease in September, I’m not sure it will happen. The producer price index came in hotter than expected this week. Fed action will depend mainly on the personal consumption expenditures index (PCE), the Fed’s favourite measure of inflation, which will be out on August 29.

US stagflation worries have emerged with the release of the July employment report, which showed considerable weakness, enough to get the head of the Bureau of Labour Statistics fired. The likelihood of a BoC cut will increase if the Fed begins a series of easing moves as the administration is demanding.

Dr. Sherry Cooper

-

Canada’s July Labour Force Survey Was the Weakest Since 2022

Canada’s July Labour Force Survey Was the Weakest Since 2022 Employment fell by 40,800 jobs in July, a weak start to the third quarter, driven by decreases in full-time work, with most of the decline in the private sector. The jobless rate held steady at 6.9%, even though the number of unemployed people fell. The monthly decline was the largest since January 2022, and excluding the pandemic, it’s the most significant drop in seven years.

The job loss was concentrated among youth ages 15 to 24 who have had a terrible time finding summer jobs this year. The unemployment rate for that group is a whopping 14.6%, the highest since September 2010 outside of the pandemic. The youth employment rate fell 0.7 percentage points to 53.6% in July—the lowest rate since November 1998, excluding the pandemic.

Trump’s tariff turmoil has halted so many crucial financial decisions. Potential homebuyers are deer-in-the-headlights despite the relatively low mortgage rates, strong supply of unsold homes, and lower prices. Potential move-up buyers similarly don’t take action despite the relatively strong bargaining power of buyers.

The employment rate—the proportion of the population aged 15 years and older who are employed—fell by 0.2 percentage points to 60.7% in July and was down 0.4 percentage points from the beginning of the year (61.1% in both January and February).

The number of employees in the private sector fell by 39,000 (-0.3%) in July, partly offsetting a cumulative gain of 107,000 (+0.8%) in May and June. There was little change in the number of public sector employees and in the number of self-employed workers in July.

The unemployment rate held steady at 6.9% in July, as the number of people searching for work or on temporary layoff varied little from the previous month. The unemployment rate had trended up earlier in 2025, rising from 6.6% in February to a recent high of 7.0% in May, before declining 0.1 percentage points in June.

Unemployed people continued to face difficulties finding work in July. Of the 1.6 million people who were unemployed in July, 23.8% were in long-term unemployment, meaning they had been continuously searching for work for 27 weeks or more. This was the highest share of long-term unemployment since February 1998 (excluding 2020 and 2021).

Compared with a year earlier, unemployed job seekers were more likely to remain unemployed from one month to the next. Nearly two-thirds (64.2%) of those who were unemployed in June remained unemployed in July, higher than the corresponding proportion for the same months in 2024 (56.8%, not seasonally adjusted).

Despite continued uncertainty related to tariffs and trade, the layoff rate was virtually unchanged at 1.1% in June compared with a year ago (1.2%). This measures the proportion of people who were employed in June but were laid off in July. In comparison, the layoff rate for the corresponding months from 2017-19, before the pandemic, averaged 1.2%.

There were fewer people in the labour force in July as many discouraged workers dropped out, and the participation rate—the proportion of the population aged 15 and older who were employed or looking for work—fell by 0.2 percentage points to 65.2%. Despite the decrease in the month, the participation rate was little changed on a year-over-year basis.

Despite continued uncertainty related to tariffs and trade, the layoff rate was virtually unchanged at 1.1% in July compared with 12 months earlier (1.2%). This represents the proportion of people who were employed in June but had become unemployed in July as a result of a layoff. In comparison, the layoff rate for the corresponding months from 2017 to 2019, before the pandemic, averaged 1.2% (not seasonally adjusted).

There were fewer people in the labour force in July, and the participation rate—the proportion of the population aged 15 and older who were employed or looking for work—fell by 0.2 percentage points to 65.2%. Despite the decrease in the month, the participation rate was stable on a year-over-year basis.

Employment declined in information, culture and recreation by 29,000 (-3.3%). In construction, employment decreased by 22,000 (-1.3%) in July, following five consecutive months of little change. The number of people working in construction in July was about the same as it was 12 months earlier.

Employment fell in business, building and other support services (-19,000; -2.8%), marking the third decline in the past four months for the industry. Employment also fell in health care and social assistance (-17,000; -0.6%), offsetting a similar-sized increase in June. Compared with 12 months earlier, employment in health care and social assistance was up by 54,000 (+1.9%) in July.

Employment rose in transportation and warehousing (+26,000; +2.4%) in July, the first increase since January. On a year-over-year basis, employment in this industry was little changed in July.

The number of jobs declined in Alberta (-17,000; -0.6%) and British Columbia (-16,000; -0.5%), while it increased in Saskatchewan (+3,500; +0.6%). There was little change in the other provinces.

Total hours worked in July were little changed both in the month (-0.2%) and compared with 12 months earlier (+0.3%).

Average hourly wages among employees increased 3.3% (+$1.17 to $36.16) on a year-over-year basis in July, following growth of 3.2% in June (not seasonally adjusted).Employment also declined in May in transportation and warehousing (-16,000; -1.4%); accommodation and food services (-16,000; -1.4%), and business, building and other support services (-15,000; -2.1%).

Bottom Line

The two-year government of Canada bond yield fell about four bps on the news, while the loonie weakened. Traders in overnight swaps fully priced in a quarter-point rate cut by the Bank of Canada by year-end, and boosted the odds of a September cut to about 40%, from 30% previously.

Oddly enough, manufacturing payrolls rose in July despite the tariffs. This was the second consecutive monthly gain for a sector that one would expect to be most affected by the trade war. Manufacturing employment has fallen year-over-year.

This was an unambiguously weak report, but it comes hard on the heels of a robust report. Averaging the two months of data suggests there is an excess supply in the economy. But we will need to see a decline in core inflation for the Bank of Canada to resume cutting interest rates.

Traders are now expecting the US central bank to cut interest rates when it meets again in September. With any luck at all, this will pressure the Bank to cut rates as well, but only if the interim two inflation reports show an improvement, and the labour market remains weak. The next jobs report is on September 5, and the Bank of Canada meets again on September 17.Dr. Sherry Cooper