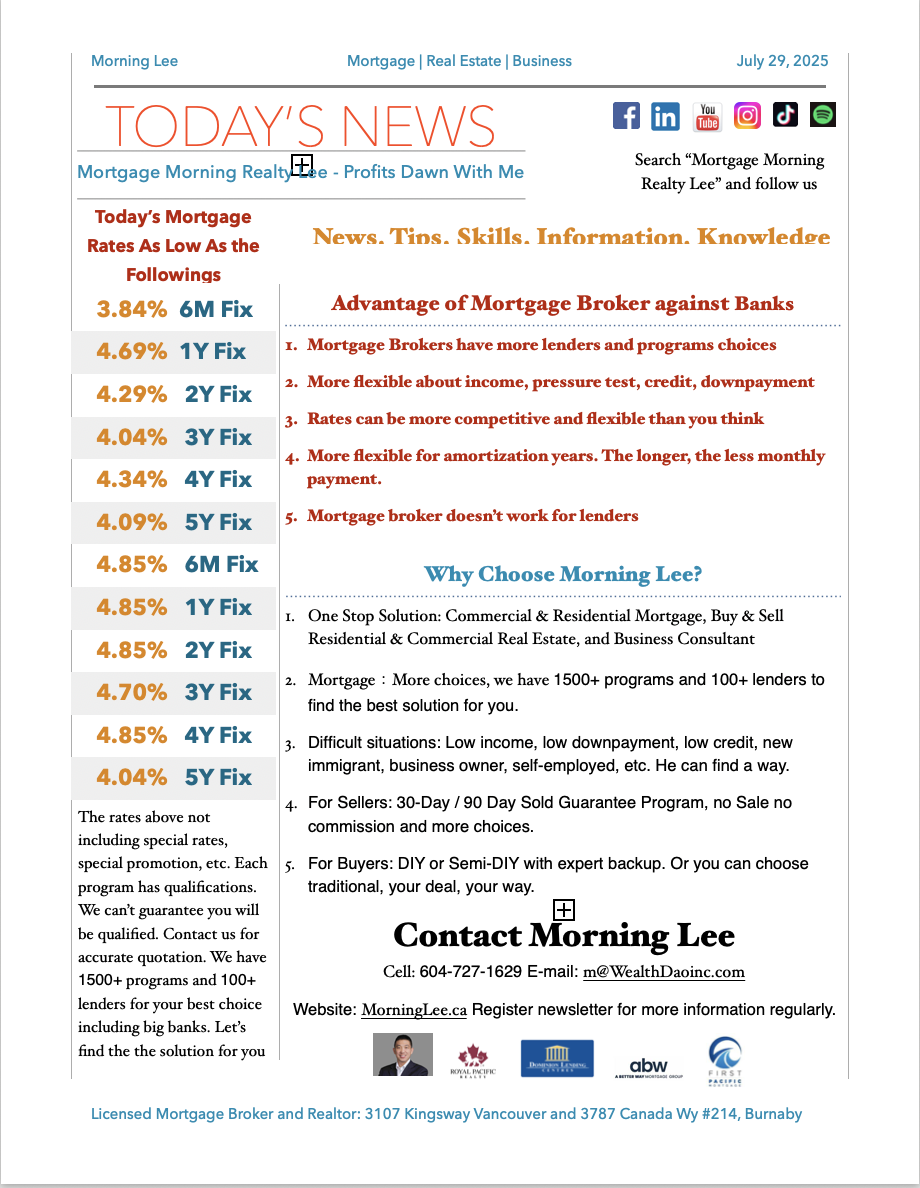

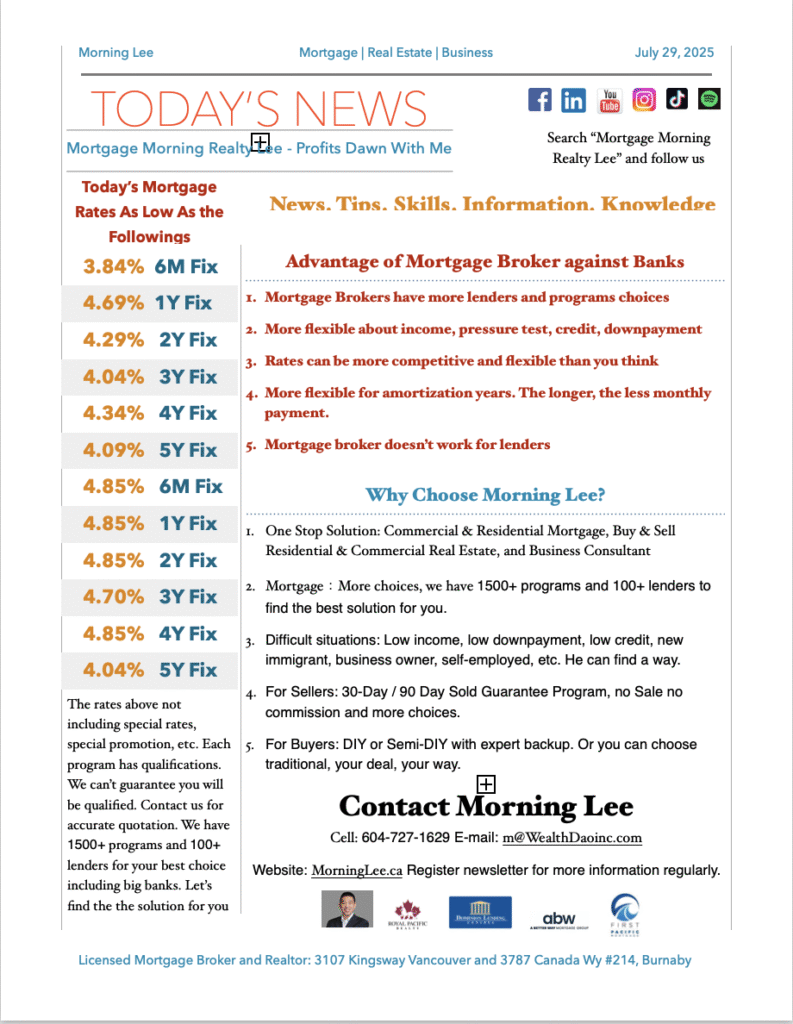

Mortgage Morning, Realty Lee – Profits Dawn with Me

Realtor, Mortgage Broker, Business Consultant

As a licensed Realtor and Mortgage Broker, with 30+ years experiences in business, real estate, and mortgage, definitely I can help you achieve your goal regarding Realty Mortgage and business.

Morning Lee – Investor / Profit Coach

Mortgage

We have different services for different requirement

Real Estate

We have different Programs For Different Situations.

- Sell Vancouver Residential Property: Single Family Home / Single House, Town House / Town Home, Apartment / Condo, Duplex / Triplex / Fourplex

- Sell Vancouver Commercial Property: Warehouse, Office, Retail Store, Industrial, Plaza / Strip Mall, Multi-Family Building, Office Building

- Sell Vancouver Business

- Buy Vancouver Residential Property

- Buy Vancouver Commercial Property

- Buy Vancouver Business

Business

Our business Consulting service focus on the following

Contact Us here if you need any help for Mortgage, Realty & Business

-

Bank of Canada Holds Rates Steady As Tariff Turmoil Continues

Bank of Canada Holds Rates Steady As Tariff Turmoil Continues As expected, the Bank of Canada held its benchmark interest rate unchanged at 2.75% at today’s meeting, the third consecutive rate hold since the Bank cut overnight rates seven times in the past year. The Governing Council noted that the unpredictability of the magnitude and duration of tariffs posed downside risks to growth and lifted inflation expectations, warranting caution regarding the continuation of monetary easing.

Trade negotiations between Canada and the United States are ongoing, and US trade policy remains unpredictable.

While US tariffs are disrupting trade, Canada’s economy is showing some resilience so far. Several surveys suggest consumer and business sentiment is still low, but has improved. In the labour market, we are seeing job losses in the sectors that rely on US trade, but employment is growing in other parts of the economy. The unemployment rate has moved up modestly to 6.9%.

Inflation is close to the BoC’s 2% target, but evidence of underlying inflation pressures continues. “CPI inflation has been pulled down by the elimination of the carbon tax and is just below 2%. However, a range of indicators suggests underlying inflation has increased from around 2% in the second half of last year to roughly 2½% more recently. This largely reflects an increase in prices for goods other than energy. Shelter cost inflation remains the biggest contributor to CPI inflation, but it continues to ease. Surveys indicate businesses’ inflation expectations have fallen back after rising in the first quarter, while consumers’ expectations have not come down”.

The Bank asserted today that there are reasons to think that the recent increase in underlying inflation will gradually unwind. The Canadian dollar has appreciated, which reduces import costs. Growth in unit labour costs has moderated, and the economy is in excess supply. At the same time, tariffs impose new direct costs, which will be gradually passed through to consumers. In the current tariff scenario, upside and downside pressures roughly balance out, so inflation remains close to 2%.

The central bank provided alternative scenarios for the economic outlook. In the de-escalation scenario, lower tariffs improve growth and reduce the direct cost pressures on inflation. In the escalation scenario, higher tariffs weaken the economy and increase direct cost pressures.

So far, the global economic consequences of US trade policy have been less severe than feared. US tariffs have disrupted trade in significant economies, and this is slowing global growth, but by less than many anticipated. While growth in the US economy looks to be moderating, the labour market has remained solid. And in China, lower exports to the United States have largely been replaced with stronger exports to other countries.

In Canada, we experienced robust growth in the first quarter of 2025, primarily due to firms rushing to get ahead of tariffs. In the second quarter, the economy looks to have contracted, as exports to the United States fell sharply—both as payback for the pull-forward and because tariffs are dampening US demand.

The gap between the 2.75% overnight policy rate in Canada and the 4.25-4.50% policy rate in the US is historically wide. Another cause of uncertainty is the fiscal response to today’s economic challenges. The One Big Beautiful Bill has passed, and it will add roughly US$4 trillion to the already burgeoning US federal government’s red ink. This has caused a year-to-date rise in longer-term bond yields, steepening the yield curve.

The slowdown of the housing sector since Trump’s inauguration has been a substantial drain on the economy. The Monetary Policy Report (MPR) for July states that “growth in residential investment strengthens in the second half of 2025, partially due to an increase in resale activity after the steep decline in the first half of the year. Growth in residential investment is moderate over 2026 and 2027, supported by dissipating trade uncertainty and rising household incomes.”

Bottom Line

We expect the Canadian economy to post a small negative reading (-0.8%) in Q2 and (-0.3%) in Q3, bringing growth for the year to 1.2%. The next Governing Council decision date is September 17, which will give the Bank time to assess the underlying momentum in inflation and the dampening effect of tariffs on economic activity.

If inflation slows over the next couple of months and the economy slows in Q2 and Q3 as widely expected, the Bank will likely cut rates one more time this year, bringing the overnight rate down to 2.50%, within the neutral range for monetary policy. Bay Street economists have varying views on the rate outlook (see chart above). While the Fed will hold rates steady today, despite the incredible pressure coming from the White House, the Bank of Canada could well cut rates one more time this year.Dr. Sherry Cooper

Chief Economist, Dominion Lending Centres -

Sell Residential Property in Vancouver? Market Signs Show It’s Turning a Corner

If you’re looking to sell residential property in Vancouver, the timing may finally be shifting in your favour. After months of hesitation, the national housing market—particularly in key metros like Vancouver and Toronto—is showing signs of a turnaround. According to a July 2025 report from MorningLee.ca, both sales and price activity have begun to stabilize, hinting that we may be entering a more balanced and predictable phase of the market.

Let’s break down what this means for sellers in Vancouver, and why some property types might have a better window to sell than others.

1. Sell Residential Property inVancouver?Why This Could Be a Turning Point for Sellers

The latest data shows that home sales rose while prices held steady in June 2025. Nationally, sales were up around 3% month-over-month, and the national sales-to-new-listings ratio rose to 50.1%—a shift toward balanced market conditions.

In Vancouver, this means buyer activity is creeping back despite ongoing uncertainty like tariff threats and fluctuating interest rate expectations. As MorningLee.ca notes, market momentum may simply have been delayed by a rocky economic spring—and is now resurfacing into the summer and fall.

2. Sell Residential Property inVancouver?What It Means by Property Type: Not All Homes Are Equal

If you’re planning to sell residential property in Vancouver, it’s essential to understand how different home types are performing:

- Single-family homes: Typically more sensitive to interest rate shifts and economic headlines, these properties may attract buyers looking for long-term stability—especially as price declines have moderated.

- Townhouses and duplexes: Often appealing to move-up buyers or downsizers, these mid-density homes could benefit from stabilizing price expectations and a tighter sales-to-listings ratio.

- Condos and apartments: While not explicitly broken down in the June report, condos tend to recover later in a cycle. Sellers should monitor interest rate moves closely, as affordability is a key factor for this segment.

If you’re unsure where your property stands in the cycle, now’s a good time to assess—not just emotionally, but strategically.

3.Sell Residential Property inVancouver?Should You List Now or Wait? A Seller’s Dilemma

The report points to cautious optimism, but also underlines continued risk: the Bank of Canada held rates steady, and bond yields have risen, suggesting fixed mortgage rates may go up again. These macro factors influence how quickly deals close, or if buyers even enter the market.

So who should act now?

- Sellers of well-located, mid-priced homes in balanced neighborhoods may benefit from limited competition, as new listings fell 2.9% in June.

- Sellers who’ve been holding off since early 2024 might consider testing the market before interest rate changes swing again.

But if your property type tends to lag in recovery cycles, or if buyer traffic is light in your area, patience may still be the better strategy. Either way, strategic timing is key—and understanding where the market cycle is headed will help you plan smarter.

The Bottom Line: Watch the Data, Move with Purpose

In a shifting market, data is your best friend. From price stabilization to listing trends, the latest report from MorningLee.ca offers a detailed pulse check on what’s real, what’s emerging, and what risks are still looming. Whether you’re a homeowner considering selling, a buyer looking to enter before rates rise, or someone navigating mortgage financing in a bumpy cycle—understanding these signals can make all the difference.

And before you make any move, make sure your property has no hidden red flags. Visit https://estatedetect.com to get an in-depth risk review before you buy or sell. Peace of mind is the best market strategy.

-

Sell Residential Property in Vancouver: 5 Easily Missed Mistakes That Cost You Thousands

When homeowners plan to sell residential property in Vancouver, their focus often falls on big-picture items—pricing, staging, and timing. But the reality? Overlooking just a few small details can quietly drain your final sale price or even kill the deal entirely.

In today’s stabilizing market, where buyers are cautious and inventory is tightening, every detail counts. Below, we break down five surprisingly common missteps sellers make—especially in the Greater Vancouver area—and how to avoid them.

👉 Read: Home Sales Rose As Prices Stabilized – Housing Market is Turning a Corner

1. Planning to Sell Residential Property in Vancouver? Don’t List with a Dirty Home

First impressions matter. And in Vancouver’s competitive market, buyers walk into an open house already comparing your home to the next five on their list. A cluttered kitchen, dusty blinds, or unkempt yard doesn’t just create bad vibes—it leads to lowball offers or buyers walking away.

Professional deep cleaning before listing isn’t a luxury—it’s part of the selling strategy. It affects perceived value and, by extension, final sale price.

2.Sell Residential Property in Vancouver Smoothly by Preparing Your Property Disclosure Statement

In B.C., the Property Disclosure Statement (PDS) isn’t legally mandatory—but buyers and agents expect it. It’s a red flag when missing. Forget to disclose past water damage or unresolved plumbing issues, and your deal may fall apart during due diligence.

To sell residential property in Vancouver successfully, your paperwork needs to be clear, transparent, and ready before listing. This is especially important when mortgage lenders get involved—missing disclosures can delay financing approvals.

3. To Sell Residential Property in Vancouver at Top Dollar, Choose Professional Photography Over Phone Pics

Think your smartphone is “good enough”? Data says otherwise. Listings with professional photos attract more clicks, more showings, and often sell for higher prices.

According to REDFIN, professionally photographed homes sold for $3,400 to $11,200 more on average than those with amateur photos. In Vancouver, where a 1% pricing shift can mean tens of thousands, this isn’t a detail—it’s strategy.

4.Sell Residential Property in Vancouver with a Suite? Know BC’s New Landlord Rules to Avoid Closing Delays

Planning to sell a home with a secondary suite (basement rental, laneway house, etc.)? B.C. has recently updated its tenancy and property-use regulations. Not understanding your obligations as a seller—especially regarding notice periods or compliance with rental bylaws—can lead to legal trouble or buyer hesitation.

If you’re listing a home with tenants, make sure you’re aligned with the Residential Tenancy Act, or you risk unexpected delays.

5. Want to Sell Residential Property in Vancouver? Understand How Empty Homes and Speculation Taxes Impact Buyer Decisions

Sellers often forget that buyers factor future taxes into their offers. The Empty Homes Tax (EHT) in Vancouver and Speculation and Vacancy Tax (SVT) in B.C. can significantly impact how appealing your property is to out-of-town or investor buyers.

Properties flagged as “vacant” or subject to speculative taxes often sit longer on the market or fetch lower bids. Transparency about current tax status is crucial.

To explore whether a property has hidden risks, we recommend tools like EstateDetect.com—a smart way for buyers to investigate before they commit.

Final Thoughts

To sell residential property in Vancouver without leaving money on the table, sellers need more than just a “For Sale” sign—they need a solid understanding of paperwork, presentation, and market trends.

Need help navigating the details? Visit MorningLee.ca to work with professionals who know how to position your home—and your loan—for success.

-

How a Vancouver Mortgage Broker Residential Specialist Can Help with Non-Traditional Down Payments

When trying to secure a home loan, most people assume the rules are set in stone: stable job, great credit, and a conventional down payment coming straight from your savings. But for many buyers in the Vancouver market, life just doesn’t work that cleanly. That’s where a Vancouver Mortgage Broker Residential professional comes in—someone who understands how to work with non-traditional down payments and align your situation with lenders that are flexible enough to say “yes.”

Vancouver Mortgage Broker Residential Insight: What Counts as a Non-Traditional Down Payment

The most widely accepted form of a down payment is your own personal savings, typically seasoned in a bank account for 90 days or more. But what happens if your down payment source doesn’t fit that mold?

Here are a few common examples of non-traditional down payments:

- Gifted funds from family

- Borrowed funds (secured or unsecured)

- Proceeds from selling assets (e.g., vehicle, cryptocurrency, overseas property)

- Business income lump sums or irregular commissions

- RRSP withdrawals under the First-Time Home Buyer’s Plan (FTHBP)

While some lenders—particularly the big five A-lenders—may flag these as unverifiable or unstable, alternative lenders and B-lenders may still be willing to work with you.

According to Canada Mortgage and Housing Corporation (CMHC) guidelines, gifted down payments must come with a signed letter and proof that the gift is non-repayable. However, not every lender interprets CMHC’s rules the same way. A Vancouver Mortgage Broker Residential expert can help match your scenario with lenders who accept these sources with fewer obstacles.

How a Vancouver Mortgage Broker Residential Expert Navigates Lender Rules for Non-Traditional Down Payments

Banks are risk-averse by design. They want your down payment to show long-term savings habits and financial discipline. In contrast, B-lenders and private lenders look at your overall risk profile more holistically:

- Is your credit score acceptable (even if not perfect)?

- Do you have a stable source of income, even if self-employed?

- Is your debt service ratio within manageable levels?

As noted in a recent market report from Today’s Report Shows Inflation Remains a Concern, Forestalling BoC Action, rising inflation and stalled Bank of Canada decisions are creating tighter conditions—but also more opportunity for flexible financing solutions, especially in non-traditional arrangements.

Top Reasons to Work with a Vancouver Mortgage Broker Residential Specialist

A Vancouver Mortgage Broker Residential advisor brings more than just connections—they bring insight into which lenders tolerate what, and how to properly document your down payment to avoid delays or denials.

1. Navigating B-Lender and Private Mortgage Options

A mortgage broker can help package your non-traditional down payment in a way that meets the documentation requirements of a B-lender or private institution. This might include:

- Drafting a gift letter correctly

- Explaining irregular deposits from a business

- Structuring short-term loans from family or friends

Each lender has their own checklist—brokers know how to meet them without triggering unnecessary red flags.

2. Reducing Rejection Risk by Pre-Vetting Your Scenario

Many buyers don’t realize they can get pre-assessed for lender fit before submitting a formal application. This helps avoid hard credit checks and mortgage declines that stay on your record for months.

If you’ve already been turned down once, a broker can also re-strategize the timing and submission of your new application. Timing matters. For example, if you’re self-employed and expecting a stronger annual income report, delaying the submission could improve your approval odds.

3. Structuring Co-Applications for Maximum Impact

Using a co-signer or spouse’s income can be a game-changer. A mortgage broker can guide you on how to present shared income without muddying the waters of liability. This is especially useful if your down payment is unconventional but your household income is stable.

Why Compliance Matters: A Vancouver Mortgage Broker Residential Perspective

It’s not enough to find a lender who might accept your situation—you also need to comply with federal regulations, such as anti-money laundering (AML) rules. This is where mortgage brokers play a crucial legal role: making sure your transaction is both feasible and compliant.

Every deposit and every transfer needs a paper trail. A good Vancouver Mortgage Broker Residential partner will ensure you stay onside, especially when using funds from abroad or sources like crypto wallets and equity sales.

Beyond Mortgages: Why Vancouver Mortgage Broker Residential Clients Need Property Risk Assessments

Finding a lender is one thing—finding a safe property is another. Many deals fall through because buyers overlook title issues, zoning problems, or hidden structural risks. Before you invest, consider running a background check on the property with EstateDetect.com—a real estate detective service that investigates potential red flags before you commit. It’s one more way to safeguard your deal from surprise issues.

Final Thoughts

Getting a mortgage with a non-traditional down payment might feel like threading a needle—but with the right support, it’s absolutely doable. A knowledgeable Vancouver Mortgage Broker Residential expert can map out your options, prepare your documents, and link you with lenders that see the full picture—not just the fine print.

To explore your options or find out if your down payment qualifies, visit MorningLee.ca and start your financing journey with a broker who actually listens.

What people say:

“As first-time buyers in Vancouver, we were overwhelmed. Morning Lee didn’t just find us the perfect Kitsilano condo within our budget, she patiently educated us every step of the way. Her negotiation skills were incredible – we got the place below asking in a competitive market! She made a stressful process feel empowering.”

Sarah T.,

Registered Nurse

Arjun P.,“Securing the right location for our expanding tech consultancy was critical. Morning Lee understood our business needs intimately, not just the square footage. She found us a strategic Gastown space with growth potential and expertly negotiated the lease terms. Her dual perspective on business and real estate is invaluable.”

Founder & CEO, NexGen Solutions

Elena R.,“Financing multiple investment properties can be complex. Morning Lee’s mortgage expertise is next-level. She secured us significantly better rates and terms than we thought possible, structuring the financing perfectly for cash flow. She doesn’t just get mortgages; she builds wealth strategies.”

Real Estate Investor

David L.,“I almost launched my e-commerce platform with costly mistakes. Morning Lee’s ‘Risk Free Startup Success’ framework (PRISMs Method) was my blueprint. Her consulting helped me validate my idea, set up efficient ops, and create a killer digital marketing launch plan. We hit profitability in Month 6 – her guidance was the game-changer.”

E-commerce Entrepreneur

Marcus W.,“We needed to refinance our manufacturing facility AND improve our bottom line. Morning Lee tackled both seamlessly. She secured optimal commercial financing, freeing up capital, then her profit consulting identified clear operational inefficiencies. Implementing her strategies boosted our profit margin by 30% within a year. A true business partner.”

Operations Director, Cascade Manufacturing

Priya S.,“Scaling my team felt chaotic until I worked with Morning Lee. Her consulting, rooted in the principles from ‘From Leadership to Success,’ transformed our culture. She helped define clear roles, implement effective communication channels, and develop a strategic roadmap everyone aligns with. Productivity and morale have soared. Essential leadership wisdom.”

Marketing Director, Bloom Creative Agency